Overview

Last week we experienced the second government shutdown in just four months. Following the approval of a spending package by Congress last Tuesday afternoon, funding for the majority of federal agencies was secured through September. However, the package only funded Homeland Security through 2/13 (this Friday). Keep in mind that Homeland Security isn’t just ICE, it also includes: TSA, FEMA, the Coast Guard and the Secret Service. Should Homeland Security fail to receive funding, there is the potential for economic consequences and travel interruptions.

As a result of the shutdown, the Department of Labor was not able to issue its report on U.S. hiring in January, as scheduled last Friday. The Bureau of Labor Statistics has rescheduled the release of The Employment Situation for this Wednesday, February 11 and CPI is scheduled to be released on Friday. Unfortunately, the disruption in jobs data comes amid uncertainty regarding the strength of the labor market amid speculation about the timing of future interest rate cuts by the Fed. Currently, the fed-funds futures market is anticipating a 25bps cut later this year in June.

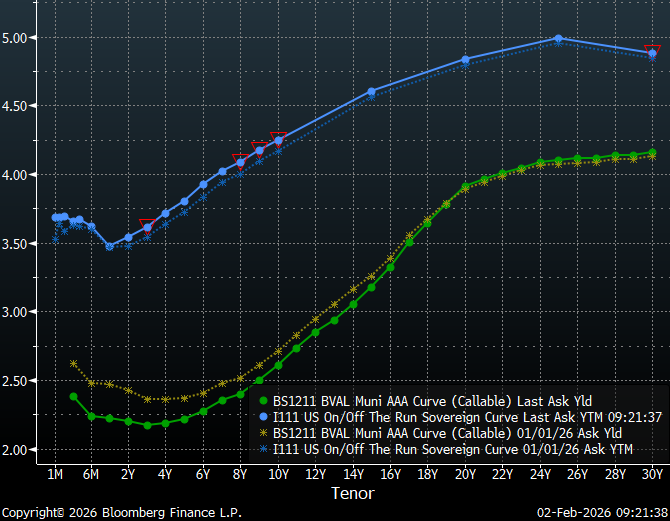

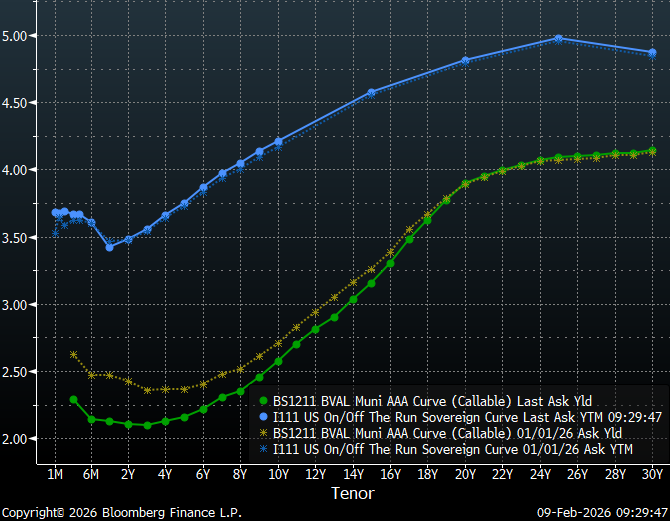

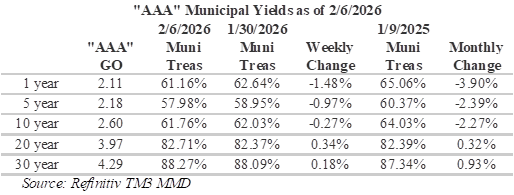

Over the past month, municipal bond yields have generally shifted lower, resulting in an overall steeper curve and shorter maturities outperforming longer maturities. The front-end of the curve has shifted lower roughly 33 bps for tenors shorter than 2-years due to strong demand from separately managed accounts and retail investors. However, Treasuries for maturities longer than 6- months have not moved meaningfully over the past month.

Insights and Strategy

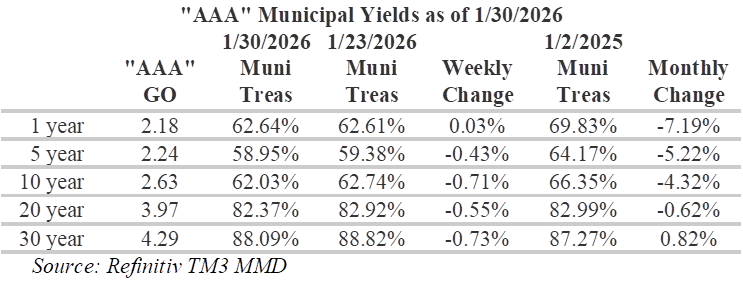

Slopes along the municipal yield curve have become consistently steep from 10 to 20-years, with 137 bps of slope compared to 49 bps from 1 to 10-years and 32 bps from 20 to 30-years. By positioning in the longer intermediate portion of the curve, investors benefit from a steep roll-down over time. Furthermore, due to flat long-term rates, municipal bond investors can currently buy maturities under 20-years that yield approximately 90% of the 30-year curve. With muni/Treasury ratios for 10-year and shorter maturities quite rich at around 60%, extending maturities further out the curve has the added benefit of more appealing relative yields. Ratios in 20-year and longer maturities remain attractive, relative to Treasuries, due to weaker demand and wider spreads. However, the yield curve remains very flat over these longer tenors. For investors seeking to maximize curve positioning with relative value, the 17 to 20-year part of the municipal yield curve has become very tempting with slopes of approximately 15-bps per year.

The municipal new issue calendar expands again this week with $13.6 billion of new issues scheduled to price. Notable issues include: the State of Washington with $1.3 billion of bonds, Houston Methodist Hospital Obligated Group has scheduled $1.26 billion, District of Columbia has a $929.6 million issue and Portland Public Schools, OR, is planning to sell $660 million. This week’s deals should see a strong reception following the second week of inflows over $2 billion with municipal bond funds receiving $2.4 billion last week, according to LSEG Lipper Global Fund Flows. Considering current muni/Treasury ratios, it is not surprising the majority of inflows are going to long-term muni funds, which reportedly received $1.8 billion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.