Overview

Although last week was a noteworthy week in terms of economic releases, yields for maturities past 6-months are largely unchanged. Last week’s economic releases included nonfarm payroll employment and the unemployment rate on Tuesday and the Consumer price Index on Thursday, hitting on both of the Fed’s primary goals of maximum employment and stable prices. Both the unemployment rate, at 4.6%, and the number of unemployed, at 7.8 million, were little changed from September. However, the current unemployment reading has crept up to the highest level seen in over 4-years. In addition, the all items CPI index, released on Thursday, surprised with a decrease in year-over-year inflation to 2.7%. The drop in inflation was largely attributed to a decline in the rent index and the owners’ equivalent rent index. It is important to note that we will have another payroll release prior to the Fed’s January meeting.

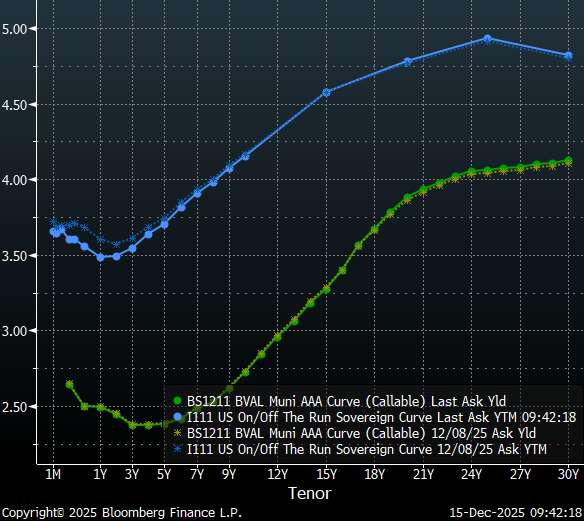

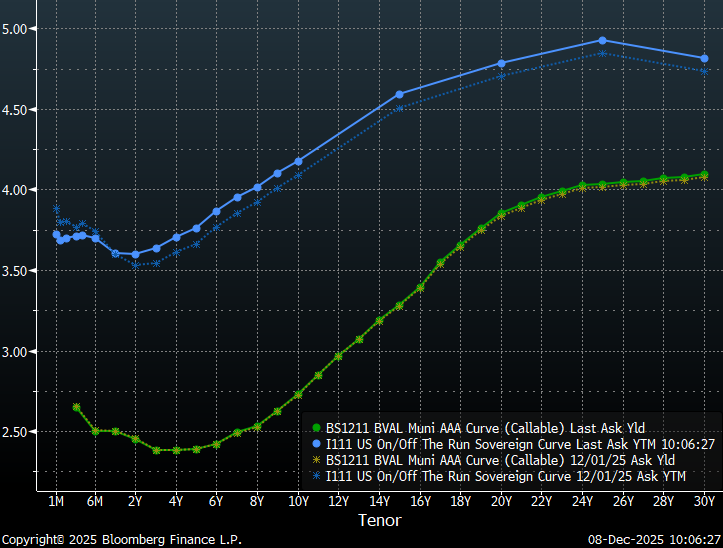

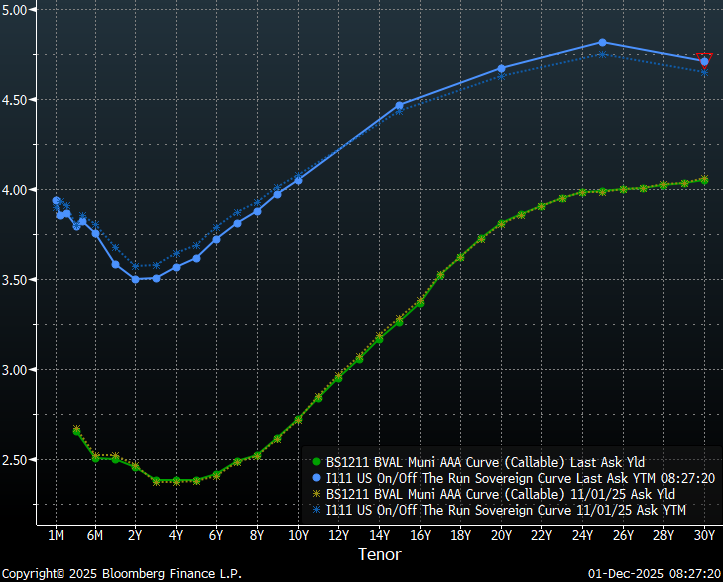

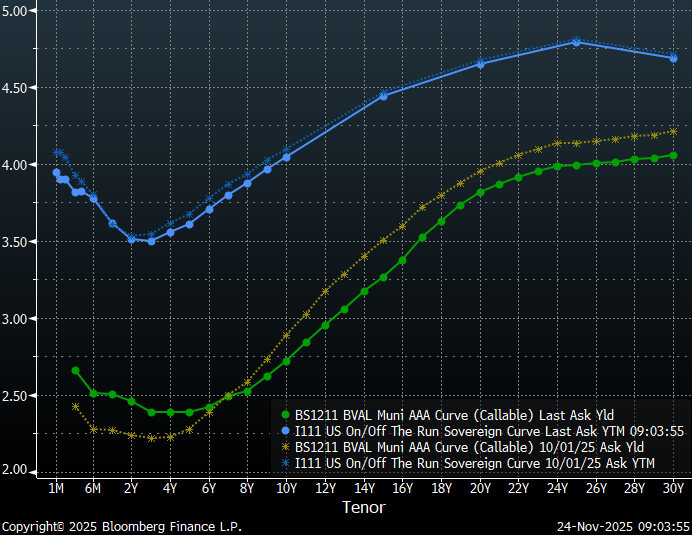

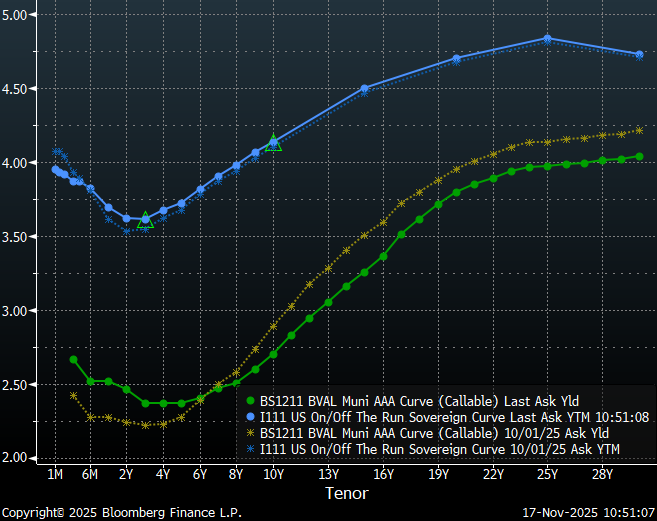

Given the mixed economic news, it is not surprising that the fixed income markets were largely unchanged over this past week. The prospect of additional rate cuts next year supports lower short-term yields, while long-maturity tenors are seeing the influence of elevated inflation expectations. But it is not just the past week that yields have held steady, even looking back two months to late October yields have been surprisingly steady. In the graph above, Treasury yields show the greatest change with modest steepening while municipals experienced relatively little change, particularly in the 5 to 20-year tenors.

Insights and Strategy

Slopes along the municipal yield curve are currently steepest around the 16-year tenor, with over 100 bps in slope from 10 to 19-years. This slope of the municipal yield curve currently rewards investors for extending from the 10-year range to the 15-20-year range. In addition, investors benefit from a steep roll-down over time. Although the municipal yield curve is currently rewarding duration, investors should be cautious when extending to maturities past 20-years, where the long-end becomes very flat. As a result of this flat tail, municipal bond investors can buy maturities under 20-years that yield over 90% of the 30-year curve.

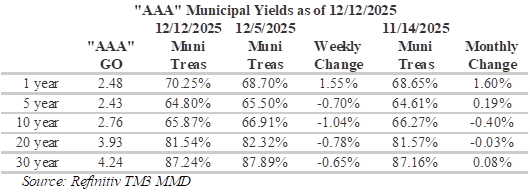

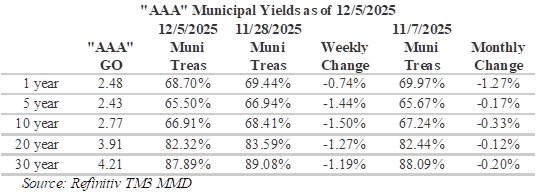

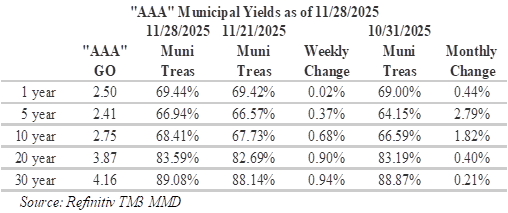

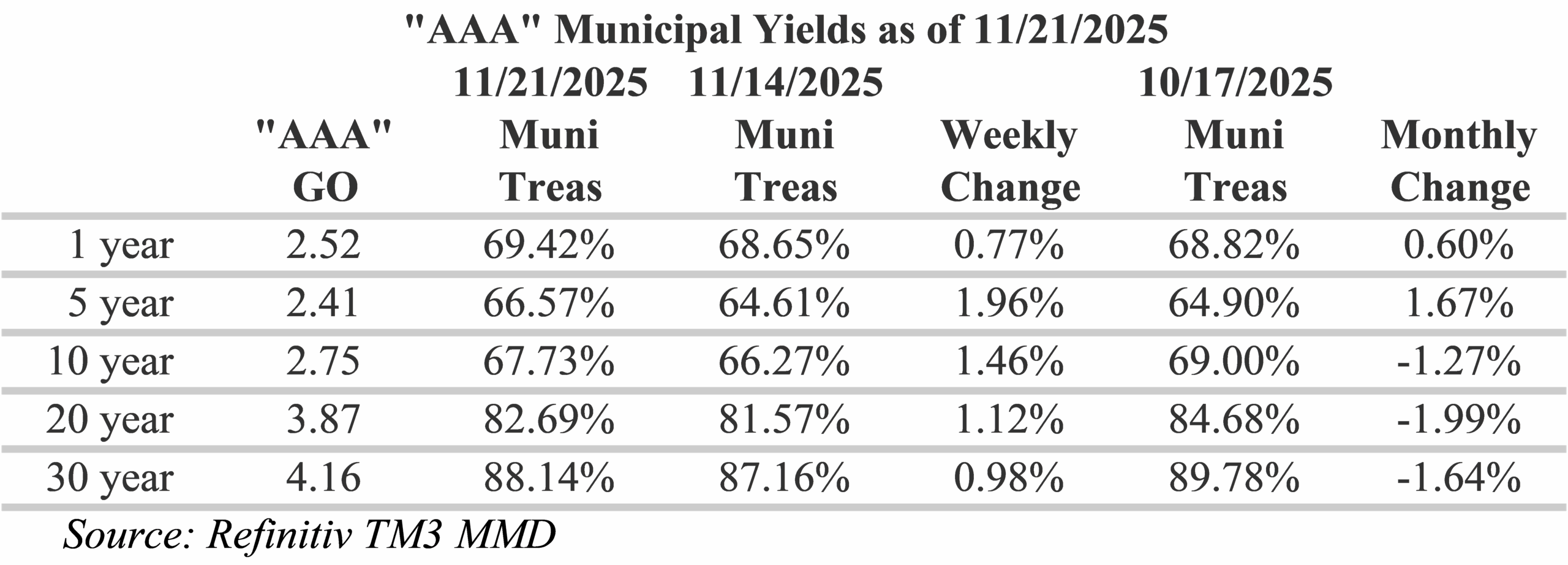

Muni/Treasury ratios have generally cheapened/increased over the past week, except around the 1-year maturity, where ratios actually decreased to just above 70%. However, this is a remarkable change from September, when ratios in the 1-year tenor dropped to as low as 56%. When combined with modest inversion over the first 5-years of the curve and more appealing ratios at the short-end, investors hiding-out in cash or spooked by inflation may be tempted by short municipals. Nevertheless, for investors seeking to maximize curve positioning with relative value, extending to the 19-year part of the municipal yield curve provides 90% of the 30-year maturity and 80% of equivalent Treasury yields.

Over the next two weeks, the new issue calendar is relatively quiet for municipals. Tomorrow, the Bureau of Economic Analysis is scheduled to release its initial estimate of GDP for the third quarter. The original report was delayed due to the government shutdown. The Bureau of Labor Services is also scheduled to release updated July, August and September PCE Inflation (the Fed’s preferred gauge) data tomorrow. Following the Fed lowering rates by a quarter point on Dec. 10 and the divided opinions within the Fed, the fed funds futures are currently pricing-in only a 20% change of the Fed cutting rates in January.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.