Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingOur team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingOur team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

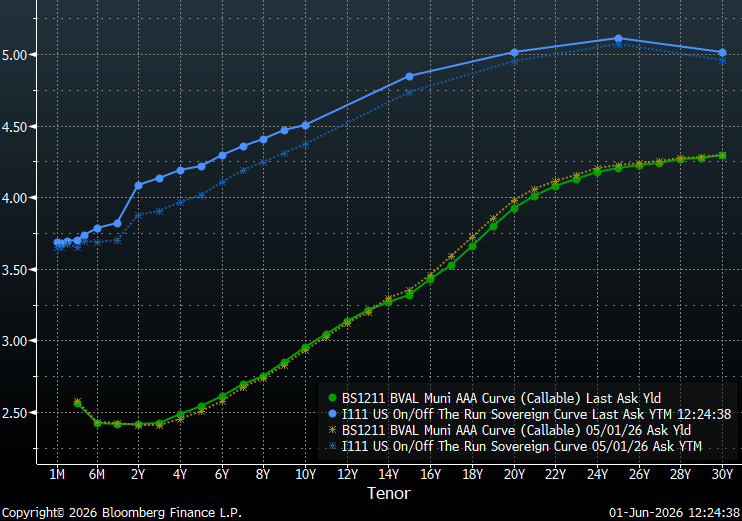

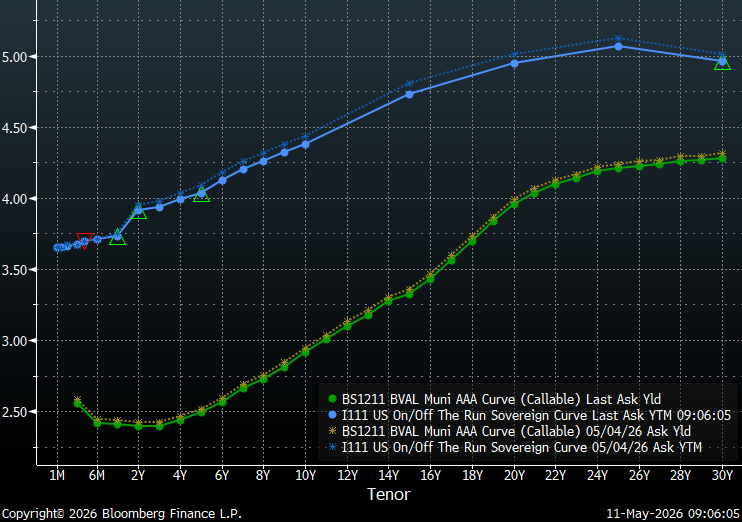

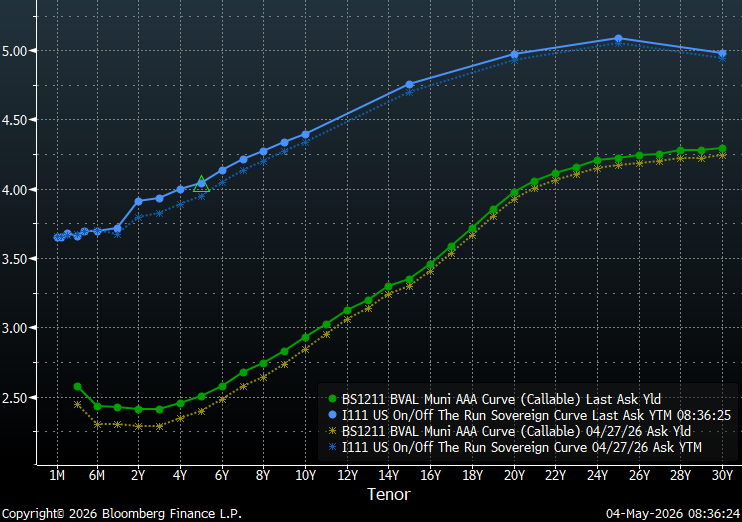

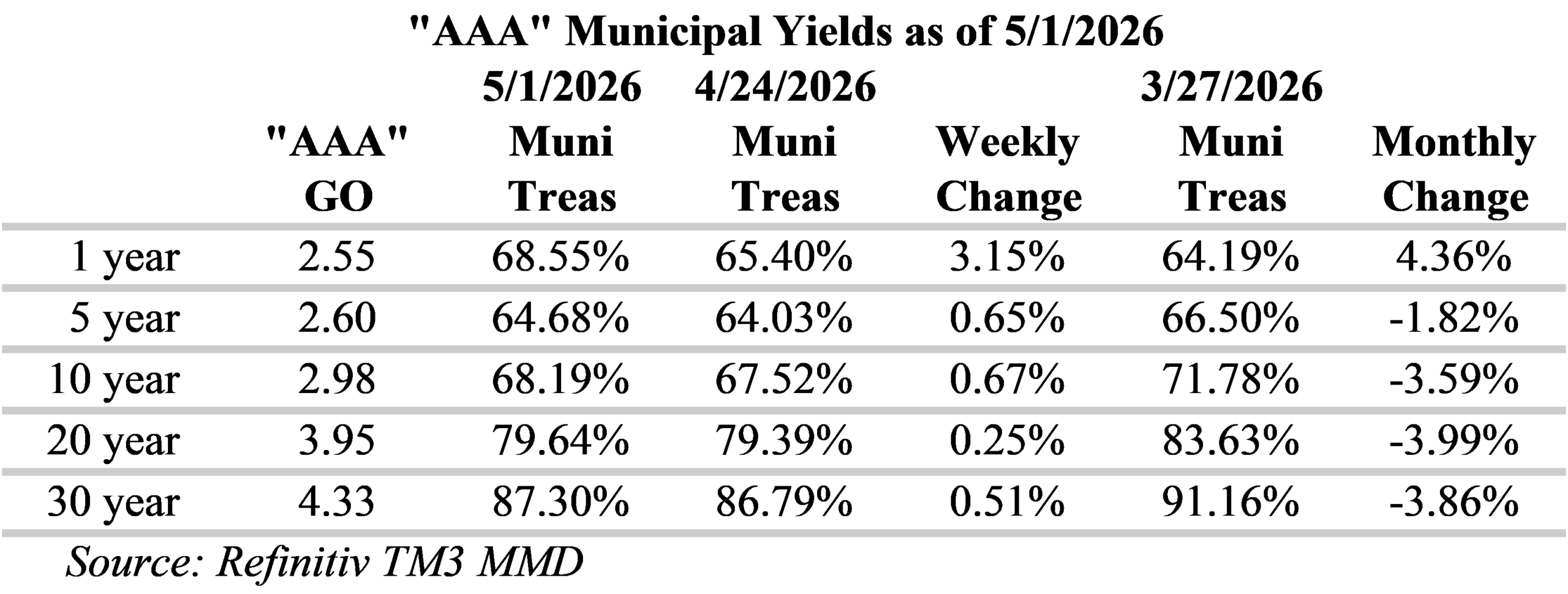

Continue readingInflation is showing signs of heating-up as the first inflation report under new Federal Reserve chief Kevin Warsh was released last week showing April consumer prices reached their highest level in almost three years. The personal consumption expenditures price index ticked-up to 3.8% for the 12-month period ended in April, almost double the Fed’s 2% target. However, this was not unexpected, as economists surveyed by Dow Jones forecasted a 3.8% rate. In the Treasury Market, inflation expectations have increased anticipation the Fed will hike rates, resulting in the gap between five-year and 30-year yields narrowing to the skinniest levels seen in more than a year. As a result, we have seen short and intermediate Treasuries underperform over the past month. However, fund flows in the muni market remain robust, with investors adding approximately $2.3 billion last week, according to LSEG Lipper Global Fund Flows. As a result, munis have held their ground better than Treasuries over the past month.

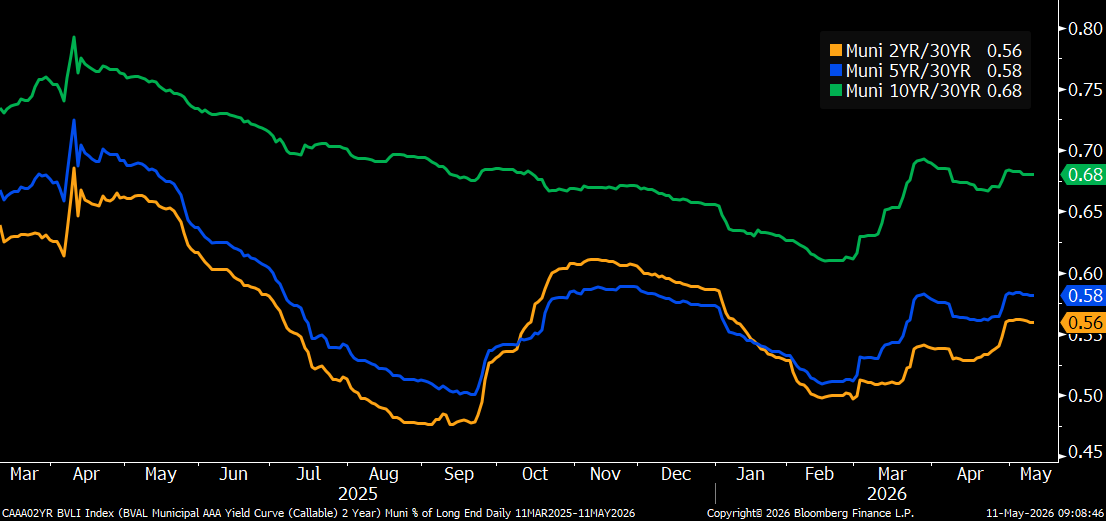

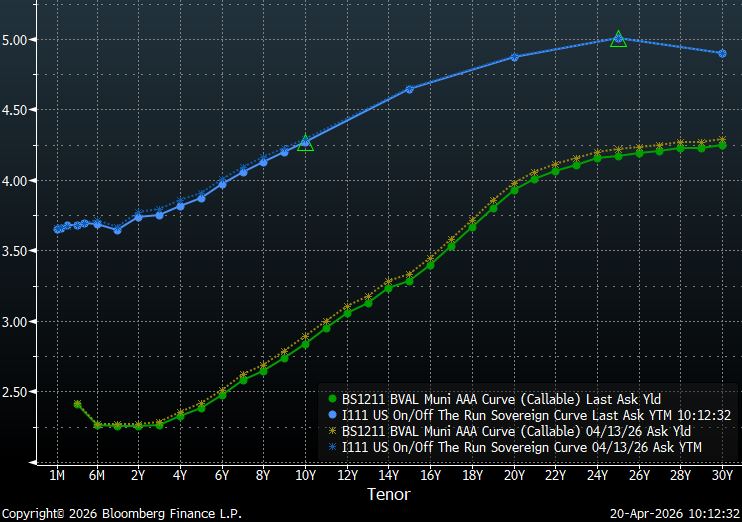

Investors continue to be incentivized to extend out the yield curve with the steepest yield slopes in the 18-21-year maturity range and an overall slope of 49 bps. However, slopes at the long-end of the municipal yield curve remain very flat with only 30 bps of slope from 21 to 30 years. Due to this flat tail, municipal bond investors can currently buy 20-year maturities that yield over 90% of the 30-year curve versus less than 70% for 10-year maturities.

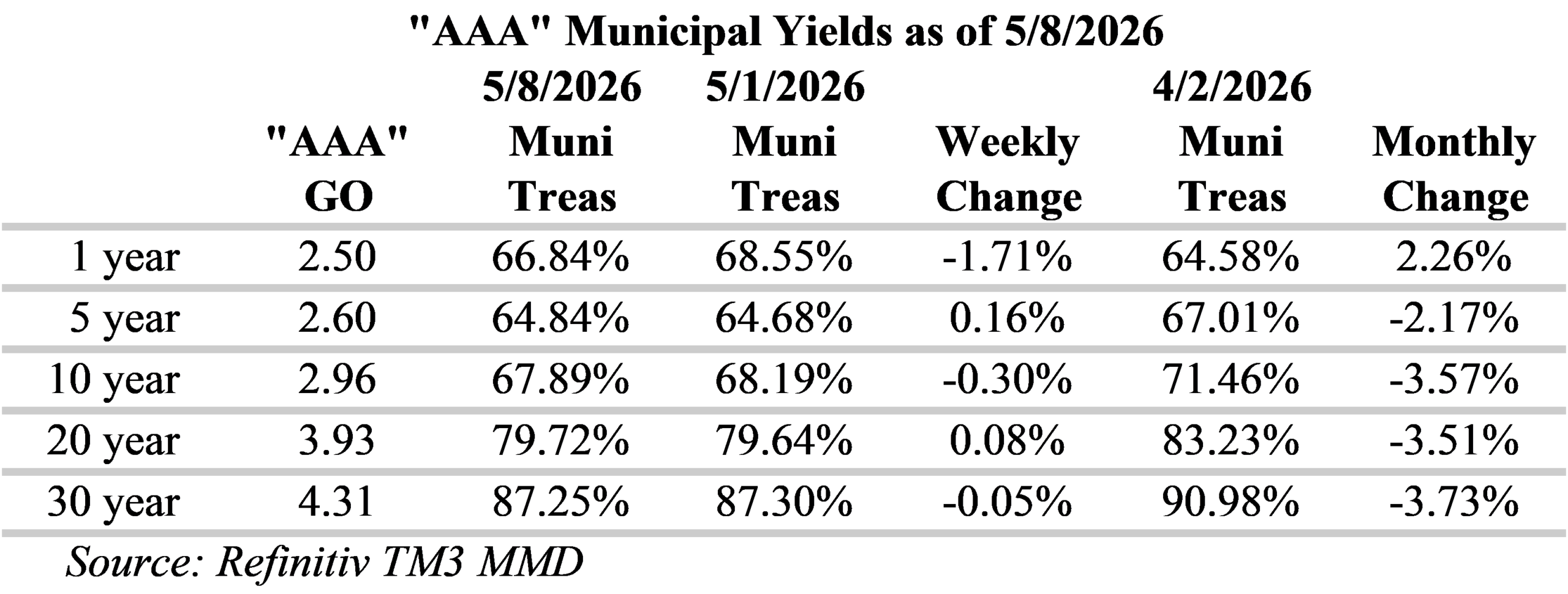

Due to the outperformance of munis, Municipal/Treasury ratios have generally declined over the past week. Municipal bonds have continued to price at richer levels as ratios fall well below several important reference points along the curve. Ratios for 10-year municipal yields are now under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 19 to 21-year part of the municipal yield curve is attractive with slopes of 11 to 13-bps per year and yields around 80% of Treasuries. Although ratios past 20-years are more attractive, relative to Treasuries, the yield curve is very flat over these longer tenors.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingHJ Sims is proud to be attending, sponsoring, and exhibiting at the National Charter School Conference.

Richard Harmon, Executive Managing Director, Head of Education Banking

Akshai Patel, Executive Vice President

John Solarczyk, Executive Vice President

Christy Meinzer, Director of Marketing, Banking and Firmwide Initiatives

Staci Webb, Senior Administrative and Operational Associate

Come visit us at booth 619 on the EXPO floor.

HJ Sims is proud to be attending the LeadingAge Virginia Annual Conference and EXPO.

Attending: Tom Bowden, Senior Vice President, David Saustad, Vice President, Steven Hicks, Vice President

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

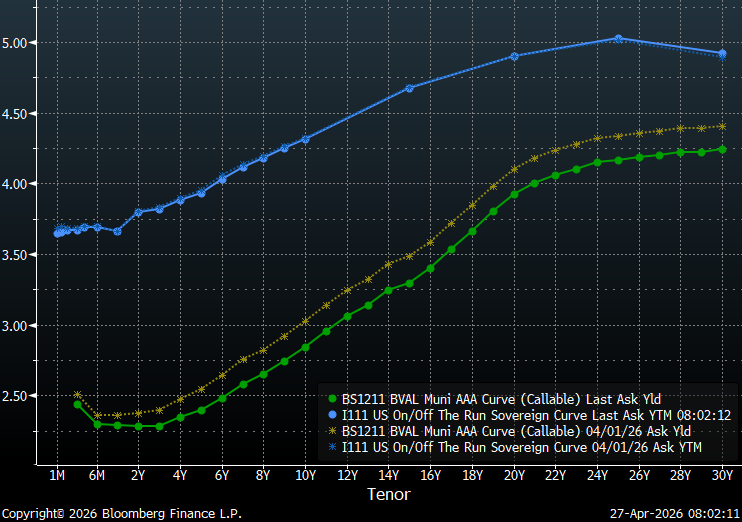

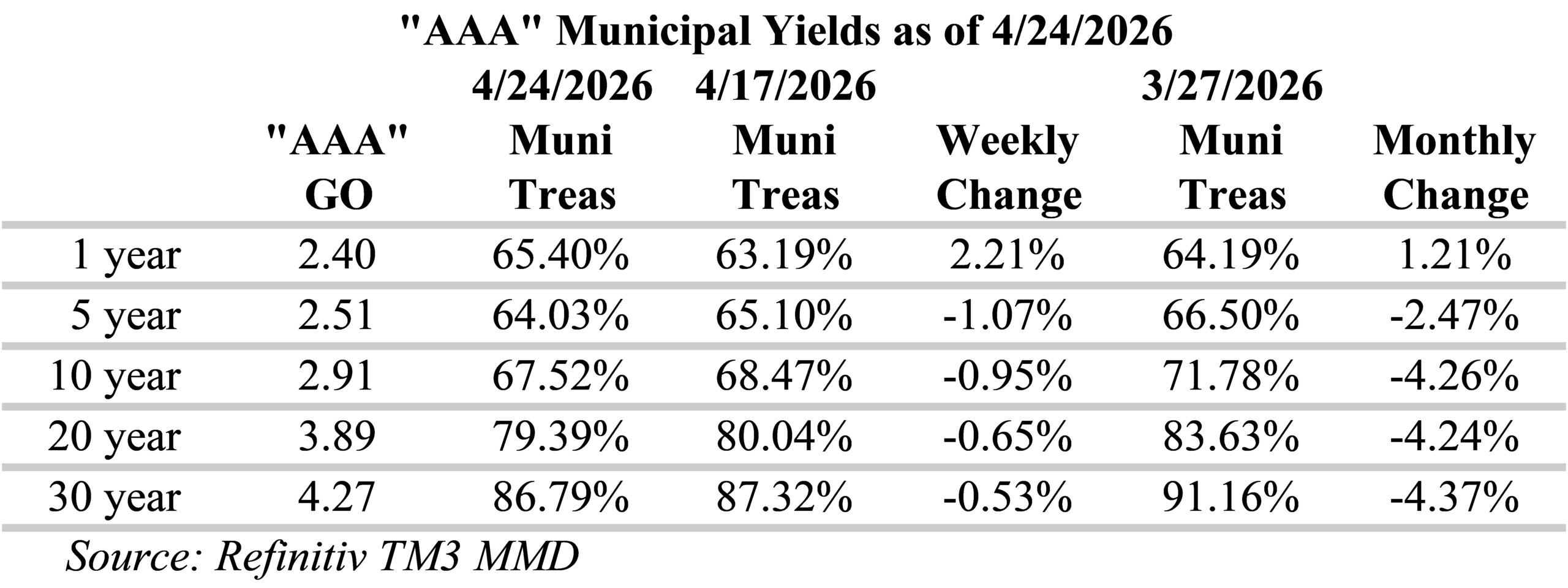

Continue readingLast week, there was a global selloff in government bonds as markets recalibrated inflation risk amid surging energy prices and speculation that central banks will tighten monetary policy. The Bureau of Labor Statistics (BLS) released its CPI report last Tuesday, which indicated that prices rose 0.6% from March and 3.8% from a year earlier. This is the highest annual reading since May 2023 and significantly above the 0.3% and 2.7% that economists had forecast. To compound matters, on Wednesday, the BLS released its Producer Price Index which showed prices climbing 6% year-over-year in April. The resulting selloff was propelled by climbing crude oil prices and a US-Chinese summit that delivered only modest results and no breakthroughs on the war in Iran. Not surprisingly, the sentiment in the Fed funds futures market has fluctuated dramatically over the past month from the Fed cutting rates to the Fed now hiking rates as soon as next March.

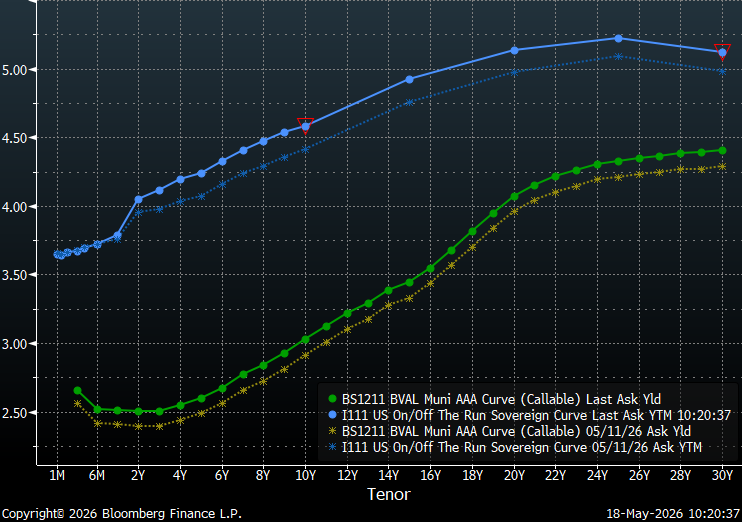

The selloff over this past week included both munis and Treasuries with Treasuries little changed for tenors under 2-years and 18-20 bps higher from five to ten years declining to 15 bps higher at 30-years. Munis generally lagged behind Treasuries with a more uniform parallel shift upward by about ten bps across the yield curve. Despite these developments, investors continue to be rewarded for extending out the yield curve with the steepest yields in the 18-21-year maturity range. The slope at the long-end of the municipal yield curve has increased past 20-years, but remains relatively flat with a total slope of 32 bps from 21-30-years. Due to this flat tail, municipal bond investors can currently buy 20-year maturities that yield over 90% of the 30-year curve versus less than 70% for 10-year maturities.

Although municipal/Treasury ratios generally declined over the past week, the short-end of the yield curve actually increased due to the muted response from Treasuries in this part of the curve. Municipal bond ratios have now fallen just below several important reference points along the curve. Ratios for 10-year municipal yields are under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 19 to 21-year part of the municipal yield curve is attractive with slopes of 12 to 13-bps per year and yields around 80% of Treasuries. Although ratios past 20-years are more attractive, relative to Treasuries, the yield curve is very flat over these longer tenors and investors are not being appropriately compensated to take the additional risk.

The municipal new issue calendar continues to be heavy this week with US state and local governments expected to sell over $11 billion of bonds. Notable deals include: the School District of Philadelphia, which plans to sell $797.5 million; Great Lakes Water Authority Water Supply System Revenue is expected to sell $754 million; Missouri Highway & Transportation Commission is on the calendar with $609 million; and, Massachusetts Educational Financing Authority is expected to bring $388.4 million to market. Despite record issuance this year, technical conditions remain supportive of the primary market. Last week, municipal bond investors added approximately $1.3 billion to municipal-bond funds, according to LSEG Lipper Global Fund Flows. Furthermore, May tax-exempt reinvestment proceeds are expected to reach approximately $34.5 billion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingThe Bureau of Labor Statistics released its Employment Situation report last Friday which reported nonfarm payroll increased by 115,000 jobs in April, despite rising energy costs from the Iran war. This is significant as the markets contemplate the future rate path of the Fed and its dual mandate to promote both maximum employment and stable prices. Collectively, the job gains in March and April mark the strongest two-month increase since 2024. Recent employment data gives the Fed justification to maintain interest rates at current levels, for the foreseeable future, while they focus on inflationary risks from rising energy prices.

Over the past week, both munis and Treasuries advanced with a modest decrease of four and a half to seven and a half basis points in Treasury yields for all but the shortest maturities. Munis lagged with a more uniform response over the week with a parallel shift downward of about three basis points. The biggest changes in Treasuries occurred in the 15 to 20-year tenor where rates fell by about seven basis points. Despite these developments, investors continue be rewarded for extending out the yield curve with the steepest yields in the 18-21-year maturity range. The muni yield curve has generally flattened over the past 3-months with short yields rising faster than longer maturities as the narrative for rate cuts and inflation has shifted. As a result, the percentage of yields relative to the 30-year curve has increased for shorter maturities. The long-end of the yield curve remains increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. Due to this flat tail, municipal bond investors can currently buy 20-year maturities that yield over 90% of the 30-year curve versus less than 70% for 10-year maturities.

Municipal/Treasury ratios have generally declined over the past week as the short-end of the yield curve declined more than the long-end. Municipal bonds have fallen just below several important reference points along the curve. Ratios for 10-year municipal yields are under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve is attractive with slopes of 12 to 13-bps per year and yields approaching 80% of Treasuries. Although ratios past 20-years are more attractively priced, relative to Treasuries, the yield curve is very flat over these longer tenors.

The Municipal new issue calendar picks-up again this week as US state and local governments are expected to sell over $13 billion of bonds. Notable deals include: the State of Connecticut, which plans to sell $1.12 billion of bonds; the City of Atlanta Water & Wastewater Revenue has scheduled $1.1 billion; the City of Boston is expected to offer $609.3 million; and, Trustees of Columbia University in the City of New York is scheduled to bring $486.9 million to the market. Despite record issuance this year, technical conditions remain supportive of the primary market. Last week, municipal bond investors added approximately $1.8 billion to municipal-bond funds, according to LSEG Lipper Global Fund Flows. Furthermore, May tax-exempt reinvestment proceeds are expected to reach approximately $34.5 billion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingLast week the Fed voted to leave its policy rate unchanged at 3-1/2 to 3-3/4 percent citing developments in the Middle East as contributing to heightened uncertainty in their economic outlook. Although this was the Powell’s final meeting serving as Fed chair, he has announced his intentions to remain on the Fed’s board after his term as chair ends. Powell could potentially remain in place as a governor until that term ends in 2028. The Fed does not meet again until June 16-17, when Kevin Warsh will host his first meeting as the new chair.

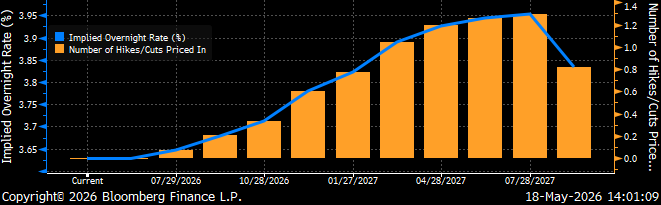

It is notable that as the market transitions from Powell to Warsh, the outlook has shifted. At last week’s meeting, four Fed officials voted against the board’s decision with objections over language suggesting the central bank would eventually resume cutting rates. Rising oil prices and a lack of progress in talks between the US and Iran has markets concerned that rates will remain higher for longer. With the Fed’s dual mandate to promote maximum employment and stable prices, the markets are concerned that policymakers will focus on oil fueled inflation rather than employment. Although the Fed funds futures market is currently anticipating that rates remain unchanged for the next 12-months, the outlook has shifted from cuts to hikes.

Over the past week, munis and Treasuries have both sold-off with rates rising anywhere from five to 13-basis points for all but the shortest maturities. The biggest changes have occurred around the policy sensitive two-to-three-year tenors while yields have risen about 5 bps for maturities past 14-years. Despite these developments, investors continue be rewarded for extending out the yield curve with the steepest yields in the 18-21-year maturity range. The long-end of the yield curve remains increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. Due to this flat tail, municipal bond investors can currently buy maturities around 20-years that yield over 90% of the 30-year curve.

As a result of the prolific short maturity bid-wanted activity, municipal/Treasury ratios for one-year and shorter maturities are meaningfully higher than they were last week with ratios over 3% higher/cheaper. Past five years, ratios slip a bit higher with demand extending out the curve to the longer maturities where relative yields are more appealing. However, municipal bonds have fallen just below several important reference points along the curve. Ratios for 10-year municipal yields remain under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve has become tempting with slopes of 12 to 13-bps per year. Although ratios past 20-years remain attractively priced relative to Treasuries, the yield curve is very flat and does not reward extension over these longer tenors.

The Municipal new issue calendar picks-up a bit this week as US state and local governments are expected to sell over $12 billion of bonds. Notable deals include: the City of Chicago Waterworks Revenue Bonds with $824.7 million, Texas State University System has scheduled $762.2 million, Chabot-Las Positas Community College District is expected to offer $531 million, and Indiana Municipal Power Agency is anticipated to bring $430 million to the market. Despite record issuance this year, technical conditions remain supportive of the primary market. Last week, municipal bond investors added approximately $615 million to municipal-bond funds, according to LSEG Lipper Global Fund Flows. Furthermore, May tax-exempt reinvestment proceeds are expected to reach approximately $34.5 billion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

HJ Sims and Sims Mortgage Funding are proud to be attending, sponsoring, and exhibiting at the 2026 LeadingAge PA Annual Conference.

Attending: Jim Bodine, Executive Vice President, David Saustad, Vice President, Stephen Anderson, Vice President, Andrew Patykula, Executive Vice President, Sims Mortgage Funding

Come see us at Booth 44!

Last week, the markets shifted their focus from day-to-day geopolitical tensions to Kevin Warsh’s testimony to Congress. The markets and Congress are both looking for indications of the independence of the Fed with Warsh acting as Chair. However, after the Department of Justice dropped its criminal investigation into the current Chair Jerome Powell, Senator Thom Tillis announced his plans to support Warsh’s nomination. It is notable that as the market transitions from Powell to Warsh, the rate-path has remained essentially unchanged. Markets are currently anticipating Warsh will proceed as the next Federal Reserve chair with his first meeting acting as Chair on June 16-17. The Fed funds futures market is currently anticipating that rates remain unchanged at this week’s meeting and for the overnight rate to remain essentially unchanged for the next 12-months.

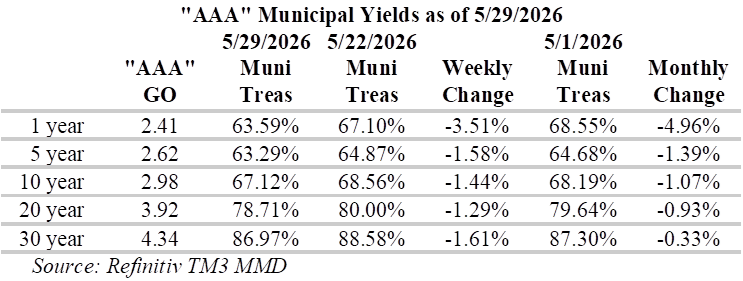

Over the last month, munis have generally outperformed Treasuries. Year-to-date, the Bloomberg U.S. Municipal Index, which includes investment grade tax-exempt municipal bonds, has returned 1.32% which has outperformed the Bloomberg US Treasury Index by 97bps. This outperformance is notable given the level of issuance, which is currently 10.5%, and relatively weak ratios in the intermediate portion of the municipal yield curve. Over the past month, Treasury yields were essentially unchanged while municipal yields fell approximately 15 to 20 bps per year from five to 30-years.

Despite recent developments, investors continue be rewarded for extending out the yield curve with the steepest yield slopes in the 18-21-year maturity range. On the long-end, the yield curve becomes increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. Due to the flat tail, municipal bond investors can currently buy maturities under 20-years that yield almost 90% of the 30-year curve.

Due largely to the prolific short bid-wanted activity, municipal/Treasury ratios for one-year maturities are meaningfully higher than they were last week with ratios over 2% cheaper for 1-year and shorter maturities. Past five years, ratios are a bit lower with demand extending out the curve to the longer maturities where relative yields are more appealing. However, municipal bonds have fallen just below several important reference points along the curve. Ratios for 10-year municipal yields are under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of equivalent Treasuries. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve has become tempting with slopes of 12 to 13-bps per year. Although ratios past 20-years remain attractively priced relative to Treasuries, the yield curve is very flat over these longer tenors.

This week, US state and local governments are expected to sell almost $10 billion of bonds. Notable deals include: Dana-Farber Cancer Institute Obligated Group, which plans to sell $1.4 billion of bonds; Texas State University System has scheduled $762.2 million; and the Los Angeles Unified School District plans to offer $650 million.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Day-to-day geopolitical tensions continue to weigh on the bond market, despite a ceasefire and the anticipated second round of peace talks. Oil prices have been very dynamic with the Strait of Hormuz effectively closed, blocking oil shipments and pressuring global prices. As a result, interest rate volatility in the bond market remains high with inflation continuing to drive rates. Although last week’s economic calendar was relatively light, sentiment drifted throughout the week between the optimism of peace talks and continued growth concerns. This week, the independence of the central bank may be tested as Kevin Warsh faces his confirmation hearing tomorrow. The hearing is particularly important because it is taking place less than a month before the current Chair’s term expires, on May 15. In addition, there is the potential for a stand-off with Republican Senator Thom Tillis vowing to block the confirmation until a Justice Department investigation is resolved.

Treasury yields were largely unchanged last week, with the biggest moves just past the policy sensitive two-year maturity as inflation, as the front end continues to be driven by inflation expectations. Munis generally outperformed Treasuries despite outflows of $427 million, according to LSEG Lipper Global Fund Flows. The biggest moves along the municipal yield curve occurred from 10 to 20-years, where the municipal curve is steepest, with yields falling roughly 5 bps in this range. On the short-end of the municipal curve, there was little change with yields slightly higher due to elevated short maturity bid-wanted activity at the tail-end of tax season.

Despite last week’s moves, investors continue be rewarded for extending out the yield curve with the steepest yields in the 18-21-year maturity range. On the long-end, the yield curve becomes increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. Due to the flat tail, municipal bond investors can currently buy maturities under 20-years that yield almost 90% of the 30-year curve.

Due largely to the prolific short bid-wanted activity, short municipal/Treasury ratios are meaningfully higher than they were last week with ratios almost 2% richer for 1-year and shorter municipals. On the long-end, ratios are a bit lower with demand extending out the curve to the longer maturities with more appealing relative yields. However, municipal bonds have now fallen just below several important reference points along the curve. Ratios for 10-year municipal yields are now under 70% of Treasuries and 30-year ratios are now below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve has become very tempting with slopes of 12 to 13-bps per year. Although ratios past 20-years remain attractively priced relative to Treasuries, the yield curve is very flat over these longer tenors.

This week, US state and local governments are expected to sell more than $10 billion of bonds. Notable deals include: the Commonwealth of Massachusetts, which plans to sell $1.09 billion of bonds; Nebraska Public Power District is scheduled to sell $829.5 million; Texas Transportation Commission is expected to offer $750 million; and, Virginia College Building Authority is expected to bring $406.2m to market. HJ Sims will also be in the market with Bonesta and its Alumus portfolio acquisition, which is expected to include $102,905,000 in Arizona and $59,725,000 in Washington and Porter’s Neck Village with $55,575,000 for its phase 2 expansion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingGeopolitical concerns continue to weigh on the bond market despite last week’s announcement of a two-week ceasefire between the US and Iran. This morning, tensions are elevated following a break-down of peace talks in Pakistan over the weekend. As a result, rate volatility in the bond market remains high with inflation continuing to pressure rates. Last week’s release of the core personal consumption expenditures index by the Bureau of Economic Analysis for February indicated an increase in prices of 0.4% from January, in-line with analyst expectations. Last Friday’s release of the consumer price index indicated that inflation surged 0.9% in March, the fastest pace in nearly four years. Furthermore, spiking fuel and fertilizer prices have economists anticipating continued inflationary pressures.

Munis outperformed Treasuries last week amid continued support as inflows of $866 million were added to municipal bond funds last week, according to LSEG Lipper Global Fund Flows. Although the Treasury market was largely unchanged with as slight sell-off past 10-years, munis rallied for all maturities across the curve with the biggest moves from five to 15-years. As a result, municipal/Treasury ratios are meaningfully lower than they were last week, with ratios generally 3% richer. Furthermore, relative yields for municipal bonds have now fallen through important reference points in several spots along the yield curve. Ratios for 5-year municipal yields are now under 65% of Treasuries and 10-year ratios are now below 70% of Treasuries. On the long-end, 30-year municipal yields have now fallen below 90% of Treasuries.

Despite last week’s moves, the steepest slopes along the municipal yield curve continue to reward extending duration. Investors are rewarded for extending out the yield curve with appealingly steep yields with the yield differential between 2-year and 10-year munis, now around 66 bps, which is over double the spread at the end of last year. On the long-end, the yield curve becomes increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve has become very tempting with slopes of 12 to 13-bps per year. While ratios past 20-years remain attractively priced relative to Treasuries, the yield curve is very flat over these longer tenors. Due to the flat tail, municipal bond investors can currently buy maturities under 20-years that yield almost 90% of the 30-year curve.

This week, US state and local governments are expected to sell more than $14 billion of bonds. Notable deals include: City of Austin Airport System, which plans to sell $1.18 billion of revenue bonds; Banner Health Obligated Group, which is scheduled to sell $990.2 million; and, Southern California Public Power Authority is expected to offer $770 million. HJ Sims will also be in the market with Lifespace Communities, Inc., which is expected to include $98,490,000 in bonds. This week, we expect the markets will be closely following the producer price index for the month of March which is scheduled for release on Tuesday.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingHJ Sims is proud to be attending the LeadingAge Indiana Spring Conference.

Attending: Lynn Daly, Executive Vice President

HJ Sims is proud to be attending and speaking at the LeadingAge Michigan Annual Conference & Solutions Expo.

Lynn Daly, Executive Vice President will be speaking on the below topic:

April 27, 2026 at 10:15am – Redefining Middle Market