Overview

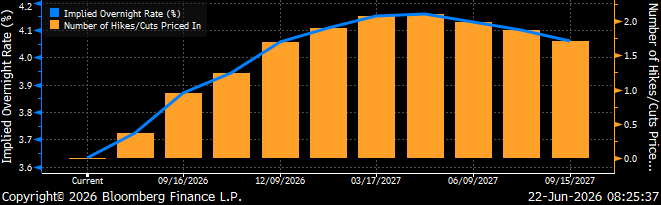

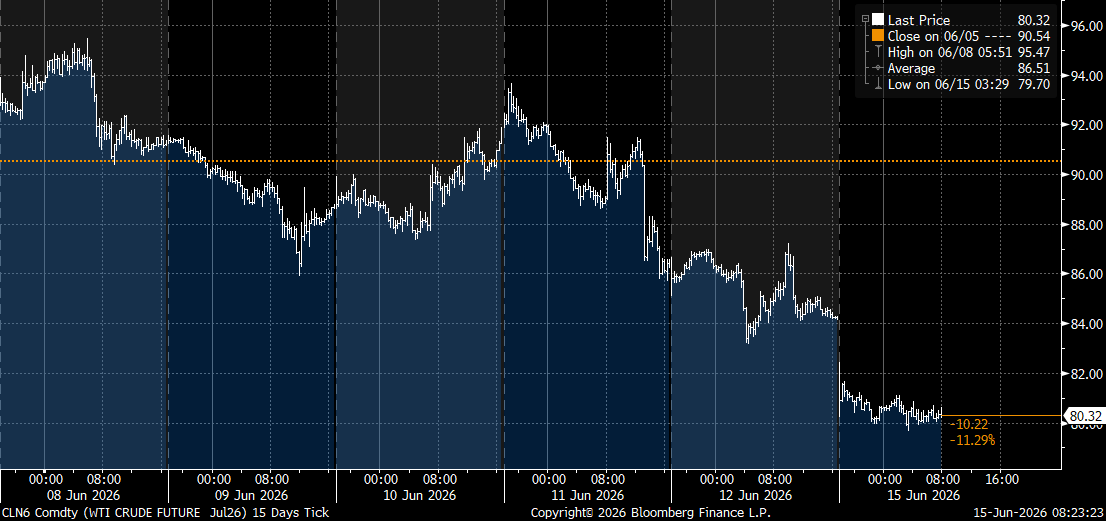

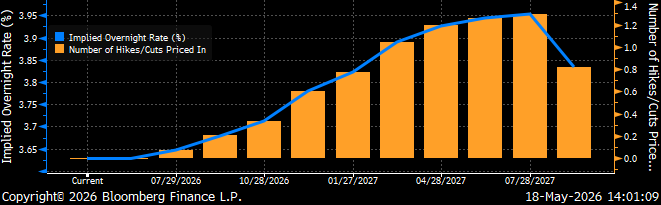

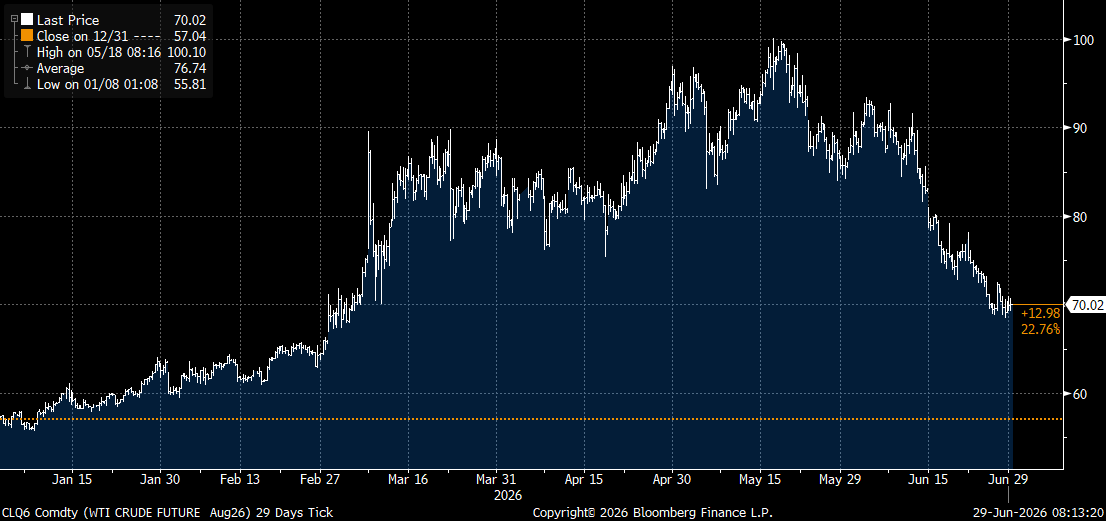

Following an escalation of tensions in the Strait of Hormuz, Iran and the US have reportedly agreed to stop mutual attacks. Although there is an agreement in place, shipowners remain wary of crossing the strait. As a result, oil prices are up again this morning and we are seeing Treasuries trade off a bit, particularly in the intermediate portion of the yield curve. While this week is a holiday week with a lighter new issue calendar, accounts are likely to be attentive with over $100 billion in combined July and August redemptions.

West Texas Intermediate Crude Futures

Insights and Strategy

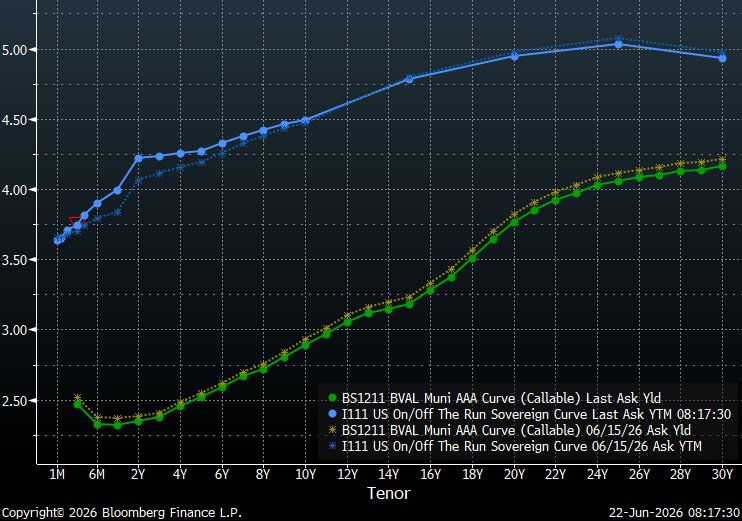

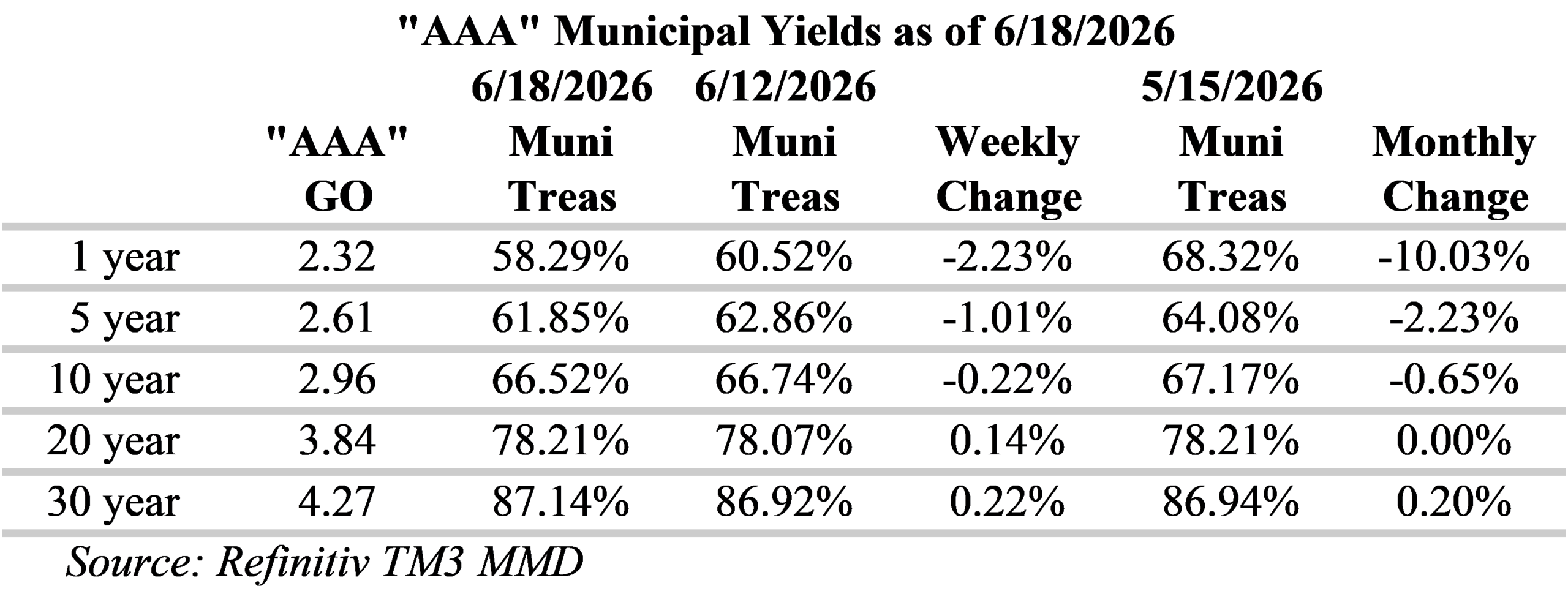

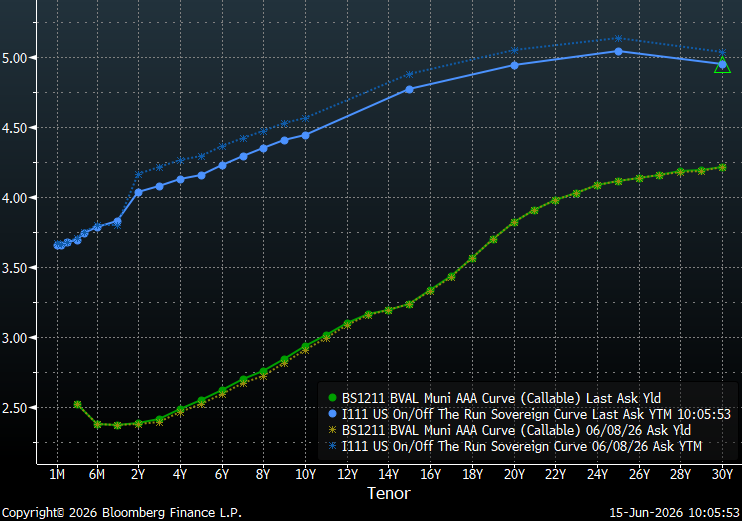

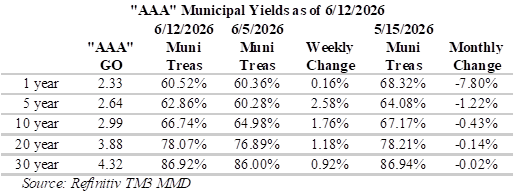

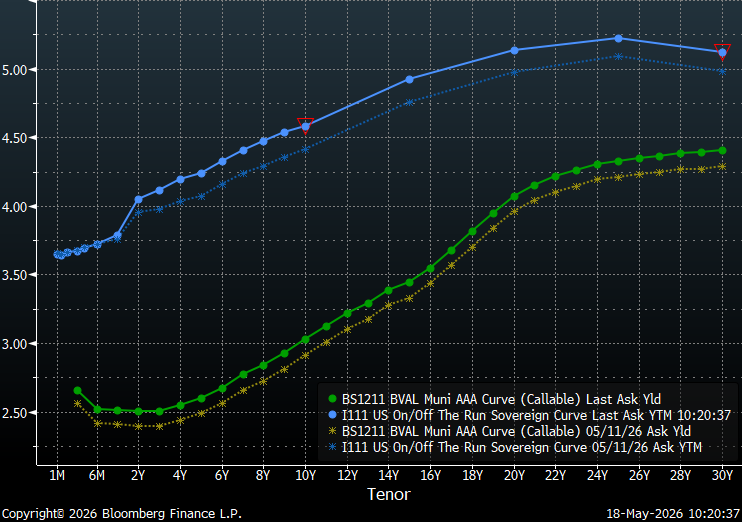

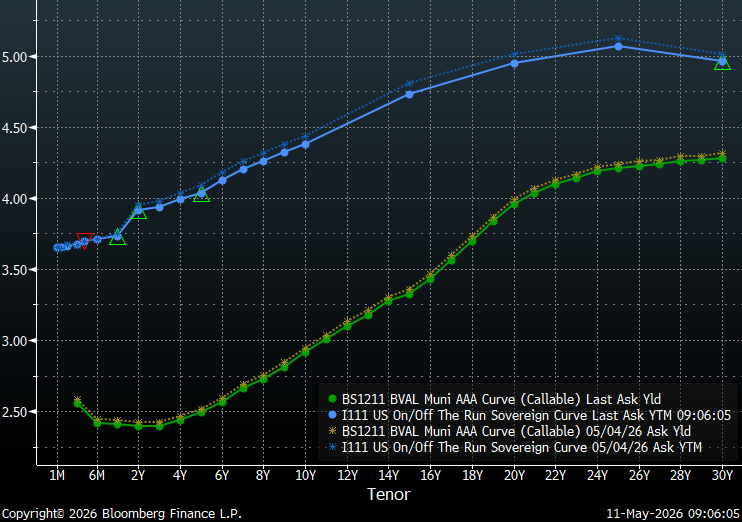

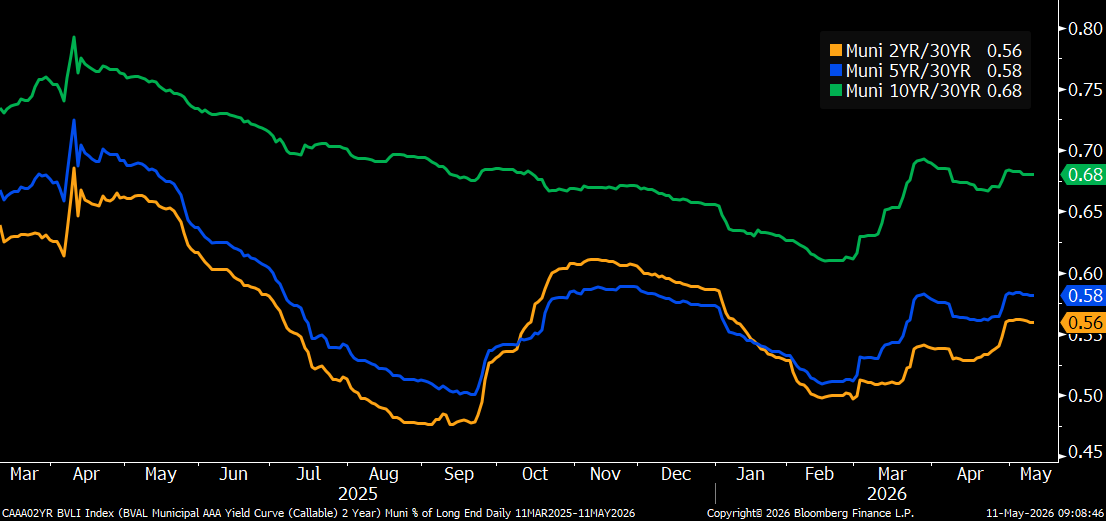

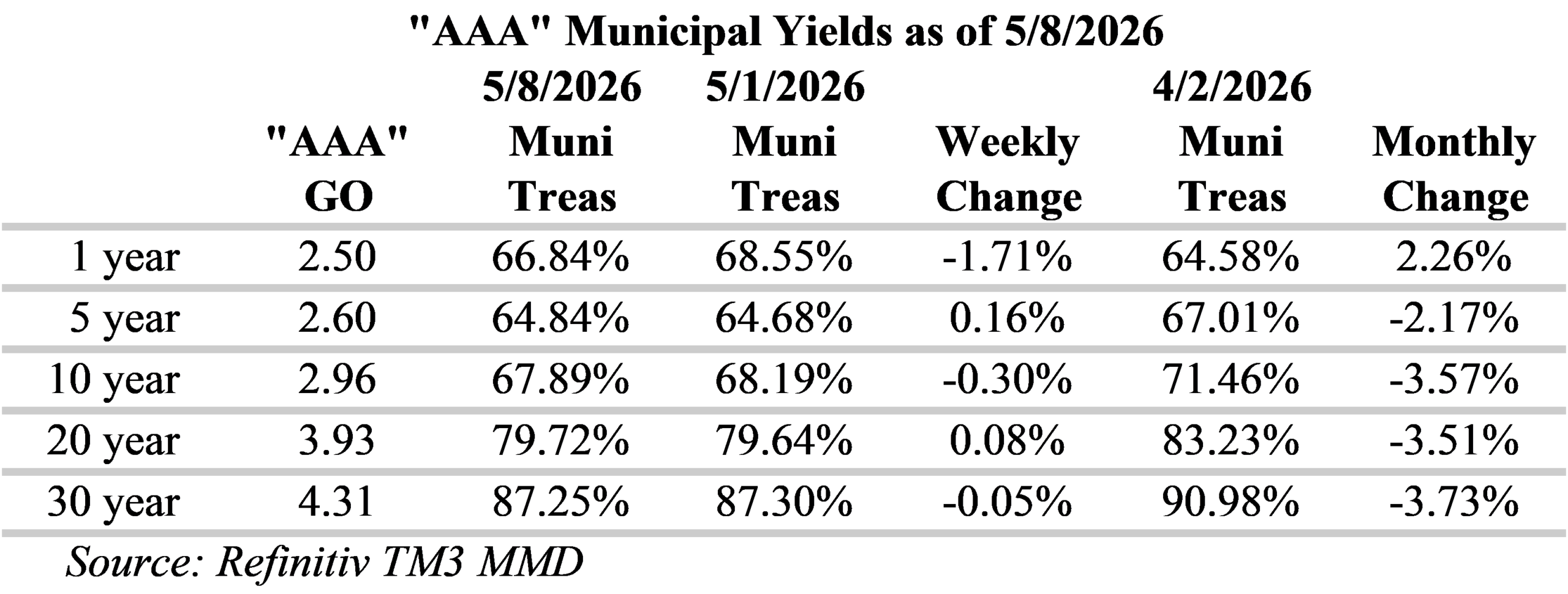

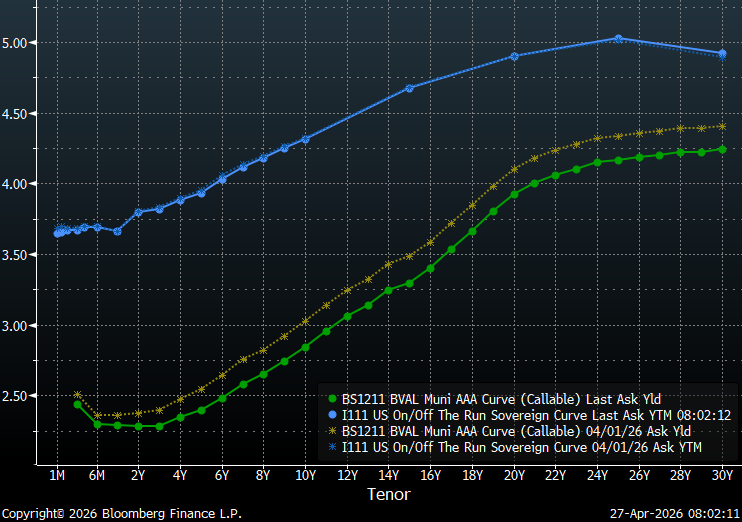

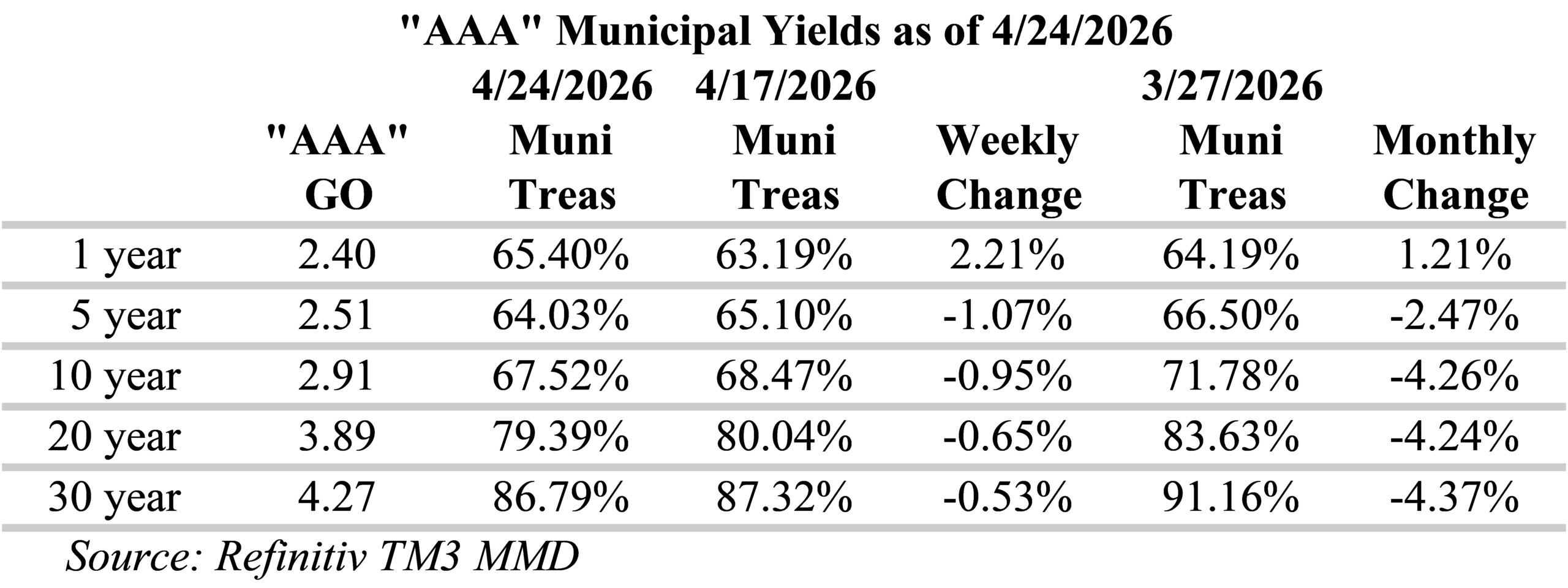

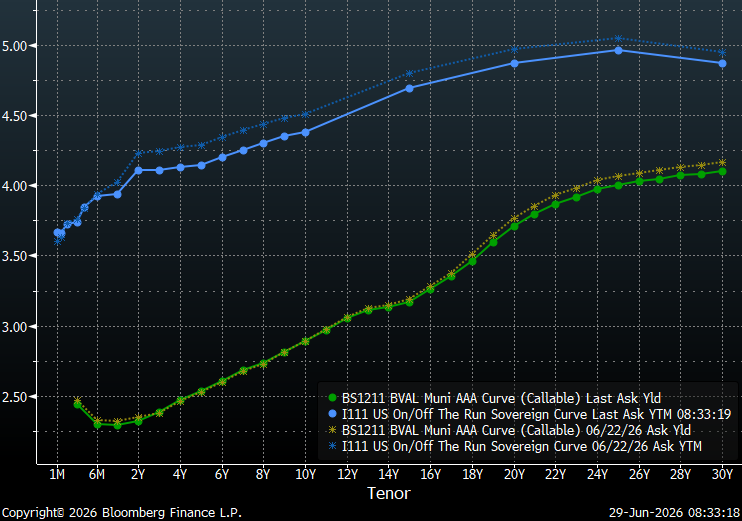

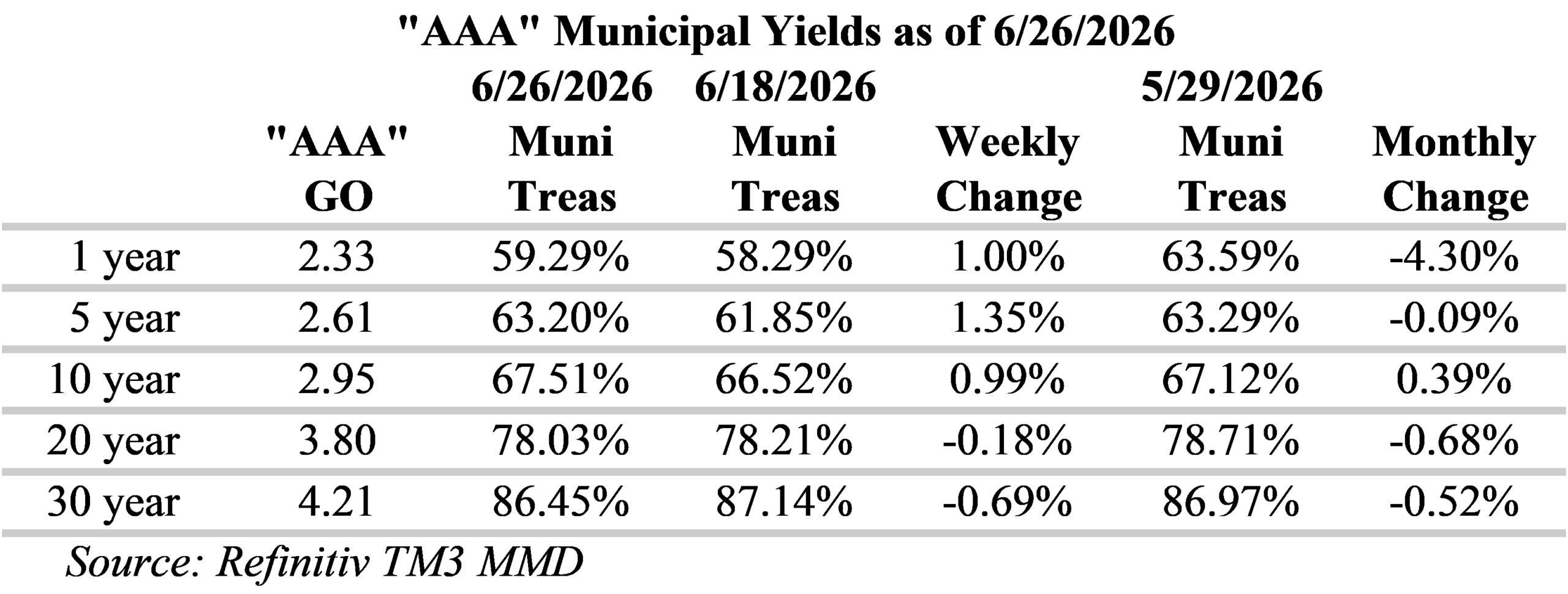

Both municipal and Treasury curves have flattened over the past week. Currently, the slope of 2 to 10-year Treasuries is less than half of what it was in mid-May and near the tightest levels seen in over a year. This flattening is the result of shorter-dated Treasuries anticipating rate hikes while longer maturities face inflation uncertainties. However, the first 6 months of the curves could not be more different, with munis inverted and Treasuries steeply upwardly sloped. Although the yield curve has flattened, Investors continue be rewarded for extending out the yield curve with the steepest yields in the 19-21-year maturity range. The slope at the long-end of the municipal yield curve, past 20-years, remains relatively flat with a total slope of 31 bps from 21-30-years. Due to this flat tail, municipal bond investors can currently buy 20-year maturities that yield over 90% of the 30-year curve versus 70% for 10-year maturities.

Municipal/Treasury ratios have generally increased (cheapened) for periods shorter than 10-years, with one-year ratios 1% higher, but still below 60% of Treasuries. Ratios on the long-end, for 20-yewars and longer, are now slightly lower. Municipals have fallen well below several important reference points along the curve. Ratios for 10-year municipal yields are now well under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 19 to 21-year part of the municipal yield curve is attractive with slopes of 10 to 13-bps per year and yields around 80% of Treasuries. Although ratios past 20-years are more attractive, relative to Treasuries, the yield curve is very flat over these longer tenors.

Due to the holiday closure later this week, the Municipal the new issue calendar is significantly smaller with US state and local governments expected to sell around $7 billion of bonds. Notable deals include: Black Belt Energy Gas District with $920 million, Massachusetts Port Authority is expected to bring $812 million, Main Street Energy Inc. has scheduled $585 million and City of San Diego Water has $429.9 million on the calendar. In addition, technical conditions remain supportive of the primary market. Last week, municipal bond investors added approximately $633 million to municipal-bond funds, according to LSEG Lipper Global Fund Flows.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.