by Gayl Mileszko

In Act 3, Scene 1 of the Shakespeare play, Prince Hamlet asked, “To be or not to be?” bemoaning the pain and unfairness of life amid a sea of troubles, but acknowledging that the alternative might be worse. Nine months into our current global calamity, enduring the “whips and scorns” of this pandemic, so many of us have weighed our chances of contracting and surviving or spreading the coronavirus against chosen behaviors. In the United Kingdom as well as the United States, some of our most recent choices involve taking one or more of the emergency use authorized vaccines. Here, the Pfizer-BioNTech and Moderna COVID-19 rollout has been underway for about a month now and 31.1 million doses have been distributed. States are individually responsible for implementing programs but priority has been given across the board to health care workers and those in long term care facilities. CVS and Walgreens are critical to the plan and they aim to make at least initial visits to nearly all nursing homes by February. Some states are already making inoculations available to those over age 65 lest we “lose the name of Action” or momentum in our struggle.

The American Health Care Association reports that about 45% of long term care workers have already been vaccinated. But surveys indicate that 29% of those who work in health care delivery settings said they would probably not or definitely not take the vaccine even if it were free and deemed safe by scientists. Hesitancy mirrors that of the general public where as many as 40% plan to wait and see or pass for now due to worries about the lack of long-term studies on side effects compounded by the need to have two doses, concerns over the type of antigen itself or misinformation about genetic impacts that messenger RNA vaccines could have, general mistrust of government and perceived profits being made by the pharmaceutical companies, and concerns about duration and effectiveness against the new and more contagious variants of the virus that have begun spreading. Refusal rates this high can certainly jeopardize our ability to achieve what many believe is the critical need: population immunity.

Unfortunately, no one is expecting the pandemic to subside by this spring. There is talk and hope of having most American citizens vaccinated by the third quarter of this year. The new administration proposes additional stimulus to speed up the testing and vaccination process. Health care providers are offering an array of incentives to employees and requirements for prospects. The U.S. Equal Employment Opportunity Commission in December released guidance stating that employers can require proof of COVID-19 vaccination from employees — with some exceptions. Dialogue in the coming months will include various “immunity passport” initiatives affecting all of us that may be highly controversial but could prove to be a first critical step in restoring a return to air travel, hotel stays, mass transit, restaurant dining, tourism, conventions, sporting events, commercial real estate, and the entire continuum of senior care from independent living to assisted living to memory care and skilled nursing.

Some parts of the economy are being permanently altered by SARS-CoV-2 as is trust in certain institutions, notably including the media. At the federal, state, community, and business/institution levels, it is extremely challenging to communicate effectively with stakeholders who have so many diverse political, legal, medical, religious, investment, and historical views. Skepticism is rampant. One recent survey by communications firm Edelman found that we not only have a pandemic but an “infodemic,” an era of information bankruptcy and poor “information hygiene”. Communications from “my employer” have now become the most trusted source of information at 61%. CEO’s must take this message to heart and redouble efforts to be transparent and to safeguard information and product quality as well as to protect and upskill workers and inform and engage their communities and investors of these efforts.

Quarterly corporate earnings reports for the most recent period have just began and analysts are scouring the last three months of performance while peppering leadership with questions on plans and forecasts for the start of 2021. Traders and investors are also carefully listening to the statements and testimony from key incoming members of the Biden Administration on the many new policy proposals and their potential market impacts. Much has not yet been “baked in” to evaluations and certain markets as the shift in Congressional leadership is still being assessed.

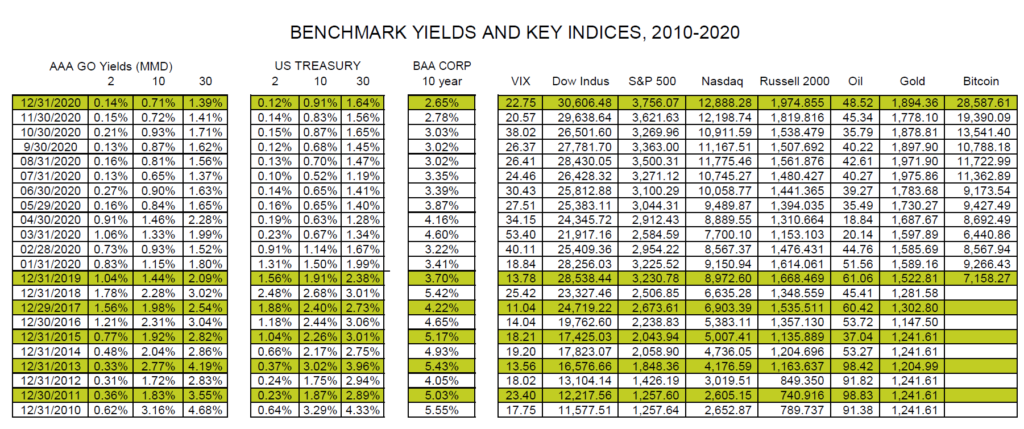

Most U.S. markets nevertheless remain on fire going on three weeks into the new year, buoyed by our central bank’s policy of unprecedented accommodation for the foreseeable future. This week’s investment grade corporate new issuance is again expected to exceed $25 billion. So far this year $22 billion of high yield corporate bonds have priced and this could be the busiest months on record for this sector. Initial public offerings proceed apace. Record inflows into high yield municipal bond funds are a perfect reflection of the ongoing demand from individuals for some tax-exempt “oomph” in portfolios that may otherwise be producing nothing more than negative real returns.

Income investors are advised to contact their HJ Sims representatives for recommendations of individual bonds tailored to their risk and capital needs profiles. The general muni market, as reflected in the ICE BoAML Index is up 0.04% this year while the HY muni index has gained 1.03%. High yield corporates are up 0.37%, and convertible bonds are returning a whopping 4.84%, primarily driven by gains in TESLA. U.S Treasuries, by comparison are down 1.15%,

We live amid a raging pandemic but the season has changed and we know that many other changes lie ahead. In many ways, we have not been down this path before. A new president is being inaugurated while an article of impeachment is pending against the former president. We have an unusually close relationship between the incumbent Chair of the Federal Reserve and his predecessor, the incoming Treasury Secretary. The central bank has the greatest single impact on markets and may use yield curve control, more liquidity support, potentially set a negative interest rate policy or exploring the use of digital currency. Major policy reversals are possible, impacting everything from taxes to health care, to energy and the environment, to immigration and corporate regulation. We may face inflation, a weakening dollar, and more horse trading than usual, given the thin margins in both the House and the Senate. We at HJ Sims wish godspeed to all assuming new public office and working to speed a recovery in each and every sector while supporting our essential services and entrepreneurs and the promising economic future ahead. As Shakespeare wrote in another famous play: “Come, love and health to all. [We] drink to the general joy of the whole table.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}