HJ Sims successfully structured and executed a $72.54 million refinancing of existing bank debt for The Legacy Senior Communities, providing stable, fixed-rate debt service for its Legacy at Midtown Park community through maturity.

Continue reading

HJ Sims successfully structured and executed a $72.54 million refinancing of existing bank debt for The Legacy Senior Communities, providing stable, fixed-rate debt service for its Legacy at Midtown Park community through maturity.

Continue reading

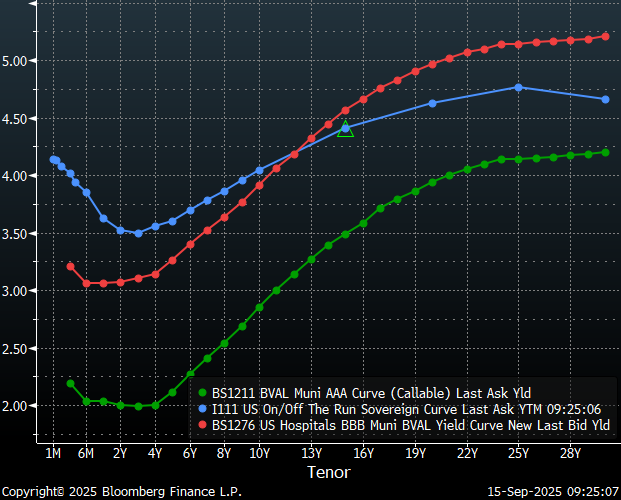

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue reading

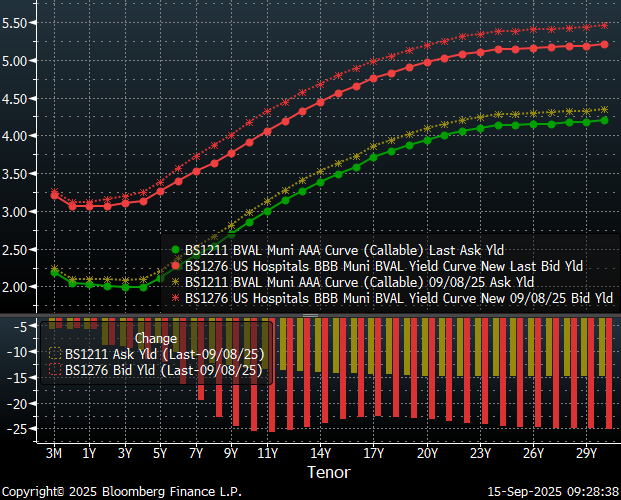

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue reading

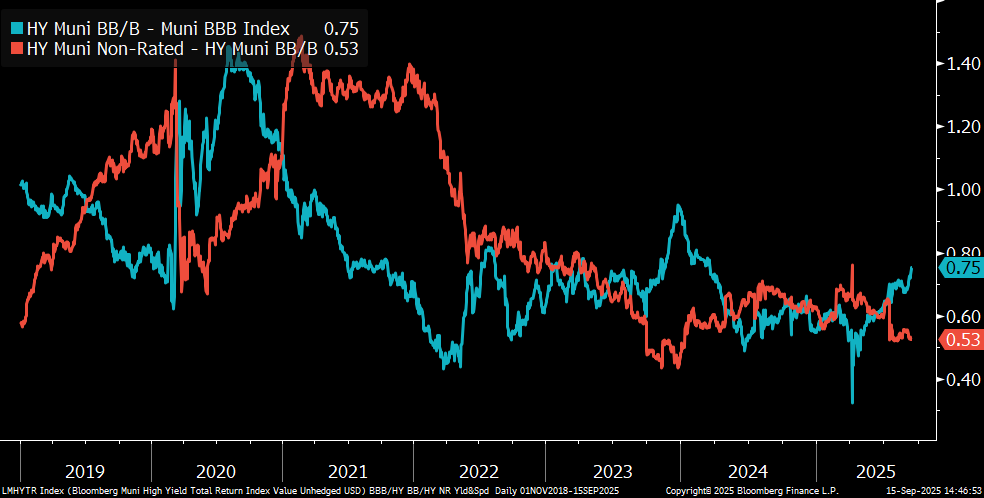

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingHJ Sims is proud to be attending, exhibiting, sponsoring and speaking at the 2025 LeadingAge Annual Conference.

Come visit us at booth 1002!

Speaking: Lynn Daly, Executive Vice President

Date: November 2, 4:30pm

Topic: Refresh and Expand Your Independent Living Offerings

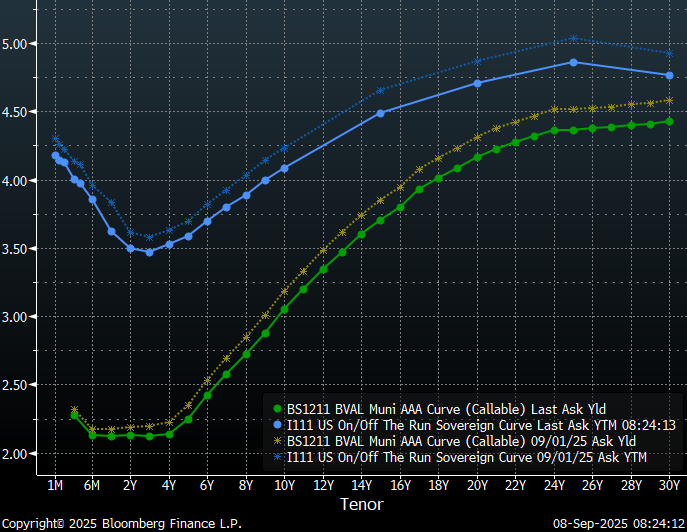

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue reading

HJ Sims Assists Elwyn With $45 Million

Financing for Milestone Master Campus

Plan Project

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingSims Partners with Pearl Healthcare to Finance Acquisition of Skilled Nursing Portfolio

Continue reading