Sims Partners with Pearl Healthcare to Finance Acquisition of Skilled Nursing Portfolio

Continue reading

Sims Partners with Pearl Healthcare to Finance Acquisition of Skilled Nursing Portfolio

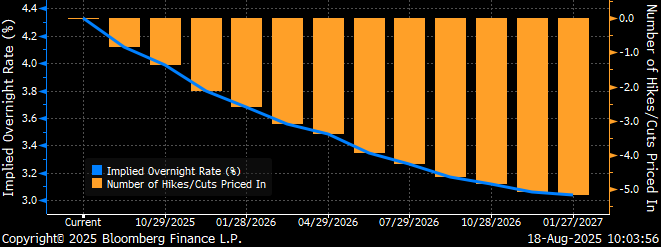

Continue readingInflation comes into a closer focus today in the Treasury market with Fed Funds Futures now reflecting an 84% chance of the Fed cutting rates next month. This is down significantly from last week when the probability was over 100%. Last week, the credit markets continued to focus on the August 1st Bureau of Labor Statistics nonfarm payrolls report, which included a cumulative downward adjustment of 258,000 jobs and convinced capital markets that a September rate cut was certain. However, the release of last week’s Producer Price Index, which jumped 0.9% on the month, compared with the Dow Jones estimate for a 0.2% gain, has markets casting doubt. Although the jobs data was striking, last week’s PPI is the biggest monthly increase we have seen since June 2022 and has the markets re-calibrating expectations.

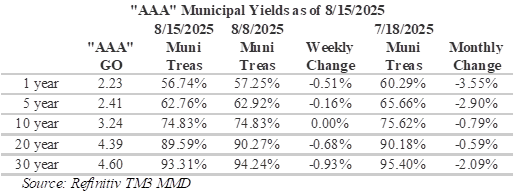

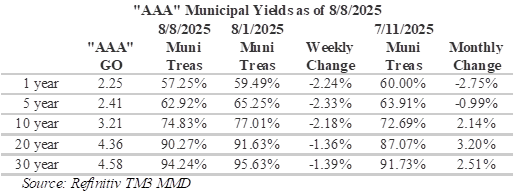

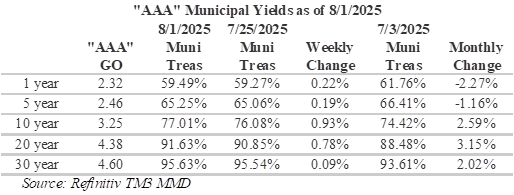

The municipal yield curve steepened a little over the past week with long maturities trending higher and maturities within 5-years rallying a bit. Treasuries also steepened over this past week, with the market selling-off as much as 8.5bpps on the long-end. On the trade desk, we continue to see aggressive bidding on the short-end with buyers continuing to anticipate a September Fed rate cut. Investors seeking optimal placement in the intermediate portion of the yield curve will be lured out to the 10-12-year tenor with relatively steep slopes and appealing yields versus the long-end of the curve. Currently the municipal curve has 52bps of slope from 2033 to 2036 with the 2036-year maturity yielding 74% of the 30-year curve. Extending an additional 7-years to the 20-year maturity brings yields to 95% of the 30-year curve. However, going much past this point marginal yields diminish to just 1- basis point per year for the last several years.

Although long-term ratios remain appealing, the yield differentials between municipals and Treasuries have once again richened over the past week. Despite the PPI recent print, muni/ Treasury ratios at the short-end of the curve continue to compress in anticipation of a September rate cut. Currently, levels are now well into to 50’s, which is a level that narrowly appeals to individual investors in the top tax brackets. While the markets have priced-in a September rate cut, the Fed remains concerned about tariff fueled inflation and sees its current policy stance as an appropriate guard against inflation. Ratios on the long-end remain relatively cheap with 20-year ratios approximately 90%.

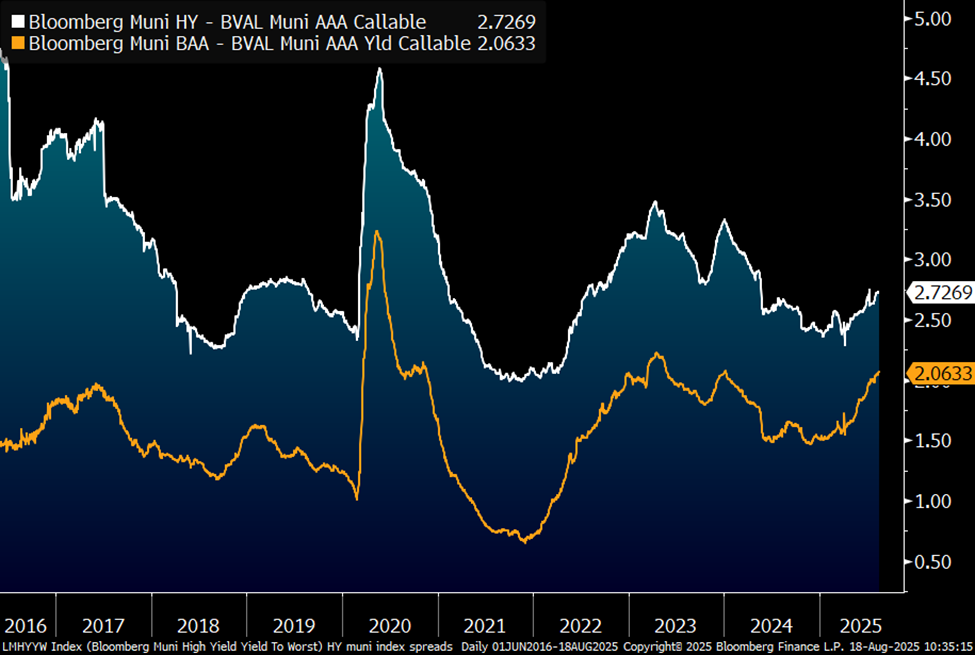

Credit spreads have been widening in the lower investment grade and non-rated sectors. Although economic concerns are weighing on the lower end of the credit spectrum, recent issuance has included several notably large non-rated and low-rated deals satisfying inquiries. Last week Florida’s Brightline private railroad rolled-over $985 million of junior debt at a yield of 14.89%. Low ridership and lagging revenue projections lead to S&P dropping its rating for some of the bonds issued on behalf of Brightline two steps to ‘BB-‘ from ‘BB+’ and Fitch lowering the senior debt to ‘B’ from ‘BB+’ at the end of last month. Recent ‘Baa’ credit spreads have widened to over 200 basis points, a 50 bps increase from the beginning of the year, and the Bloomberg High Yield municipal bond index is over 270 basis points wider than ‘AAA’ equivalents, a 40bps increase from early April following Liberation Day.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

HJ Sims is proud to be attending, sponsoring and presenting at the 2025 CSDC Conference.

Attendees: John Solarczyk

Speaking details will be forthcoming.

Start a Conversation:

HJ Sims is proud to be attending and sponsoring at the 2025 Texas Charter School Conference.

Attendees: Robert Nickell, Akshai Patel, Liam Leonard, Staci Webb

Start a Conversation:

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue reading

HJ Sims is pleased to announce our 2025 Private Wealth Management Summit. The internal Summit will be hosted on October 27th through October 30th at The Omni Grove Park Inn & Spa in Asheville, NC. This year’s program will focus on alternative investments, an increasingly relevant area in private wealth management.

The Summit offers HJ Sims financial professionals the chance to connect, learn, and exchange insights through educational sessions, collaborative discussions, and shared experiences. Together, we aim to deepen industry expertise and strengthen our ability to serve clients at the highest level.

Let us know if you will be there! Fill out the following form to RSVP to the Summit. Please let us know your check-in & check-out dates if you will need a hotel room (Marketing will coordinate hotel rooms for all attendees – you will not need to book your own room).

The information contained herein is subject to change without notice. Under no circumstances shall this constitute an offer to sell or solicitation of an offer to buy. Investments involve risk including the possible loss of principal. HJ Sims is a member of FINRA and SIPC, and is not affiliated with The Omni Grove Park Inn & Spa, NexPoint, Eagle Point Securities, Skyway Capital Markets, Preferred Capital Securities, Leon Capital Group, or Stockbridge Capital Group.

HJ Sims is proud to be attending, sponsoring and speaking at the 2025 AJAS CFO Summit.

Aaron Rulnick, Managing Principal, will be presenting on the topic below:

Presentation Title: CFO Panel Discussion : What’s Needed for Growth?

Date and Time: September 4, 2025 at 9am

HJ Sims is proud to be attending and speaking at the 2025 LeadingAge Wisconsin Annual Conference.

Speaking Details:

Lynn Daly, Executive Vice President

Date/Time:

September 11, 2025 at 8:00am-9:00am CT

Topic: If you’re not at the table, you’re probably on the menu: Preparing your board for M&A Opportunities

Start a Conversation: [email protected]

The municipal yield curve steepened over the past week with a rally in the muni market driving yields down across the curve amid aggressive bidding on the short-end in anticipation of a September Fed rate cut. Inquiries on the trade desk continue to be concentrated within 10-years and maturities under 5-years are pricing at notably tight levels. Treasuries, in contrast, flattened over the past week with the market selling-off from 6-months to 30-years with yields rising with greater consequence on the short-end than the long-end. The August 1st Bureau of Labor Statistics nonfarm payrolls report continues to weigh on the markets with traders focusing on softer payrolls data as justification for the Fed to cut rates at its next meeting. In addition, the nomination of Council of Economic Advisers Chairman Stephen Miran to serve out the final few months of Adriana Kugler’s seat following her surprise resignation last week has been viewed by the markets as a potentially dovish development.

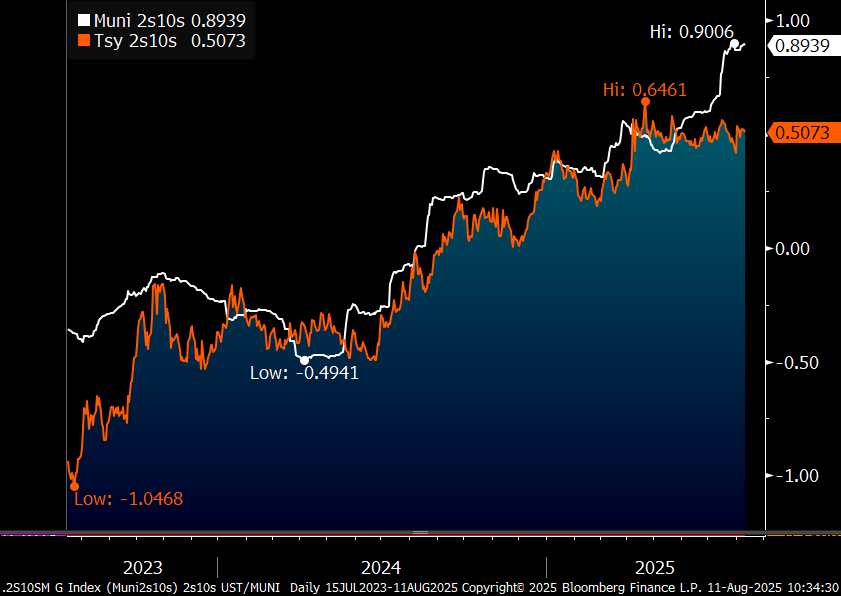

Today, the municipal yield curve continues to price to richer levels with bumps on the short-end as the long-end remains relatively cheap. Curve slopes in the more intermediate range continue to steepen with muni 2s10s continuing to steepen as the flattening treasury curve and steepening muni curve diverge. Recent movements highlight the uncorrelated nature of the two asset classes as a benefit of adding munis to fixed income portfolios. Investors seeking optimal placement in the intermediate portion of the yield curve will be lured out to the 11-13-year tenor with relatively appealing yields and steep slopes versus longer maturities. Currently the municipal curve has 80bps of slope from 8-13 years with the 13-year maturity yielding 80% of the 30-year curve. Extending an additional 7-years to the 20-year maturity brings yields to 95% of the 30-year curve. However, past this point marginal yields diminish to just 1- basis point per year for the last several years.

Although long-term ratios remain appealing, the yield differentials between municipals and Treasuries have richened over the past week. Muni/Treasury ratios at the short-end of the curve continue to compress in anticipation of a September rate cut. Currently, percentages are now well into to 50’s, which is a level that mainly appeals to individual investors in the top tax brackets. Although the markets have priced-in a September rate cut, the Fed has not been shy about concerns regarding tariff fueled inflation and sees its current policy stance as an appropriate guard against inflation. However, ratios on the long-end remain relatively cheap with 20-year ratios in the 90’s. Although risks and rewards need to carefully evaluated, the municipal yield curve is currently rewarding extension.

Last week, long-term municipal issue volumes hit $21.7 billion, which is the biggest weekly total since 2017, while steady inflows and a supportive interest-rate backdrop drove a modest rally. LSEG Lipper Global Fund Flows reported that over $2.6 billion have been added to municipal bond mutual funds over the last 2-weeks. This week municipal bond issuance is expected to be less than half of last week at $10.4 billion with $1.14 billion expected to be sold by the Port Authority of New York & New Jersey and $750 million from Long Island Power Authority. In addition, this week’s CPI data is facing heightened scrutiny by market participants following the removal of the US Bureau of Labor Statistics Commissioner earlier this month. This week’s CPI could prove pivotal amid anticipation that CPI shows inflation moving further away from the Fed’s 2% target.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

Our team of market analysts have a singular mission: to help you make better investment decisions. Read the latest market commentary.

Continue readingWith the August 1 tariff deadline, a full economic calendar and an FOMC meeting, last week was bound to be a dynamic week. However, it was Friday’s nonfarm payroll report that proved most impactful. Total nonfarm payrolls disappointed with little change reported in July with an additional 73,000 jobs, well below Dow Jones’ expectation of 100,000. Furthermore, the unemployment rate ticked up to 4.2% alongside another decrease in the labor force participation rate. However, the revisions to May and June were more impactful, with totals revised sharply lower, by a combined 258,000 jobs from previously announced levels. Markets subsequently repriced the policy outlook for the Fed’s next rate cut with the futures market pricing in the probability of a September rate hike over 90%. The news was promptly absorbed by the municipal yield curve without prejudice of maturity, with a 7 bps bump per year from 2026 to 2055, resulting in a parallel drop lower in yields. The Treasury market also responded with yields dropping, largely in the policy sensitive 2-year note, which fell as much as 28 bps.

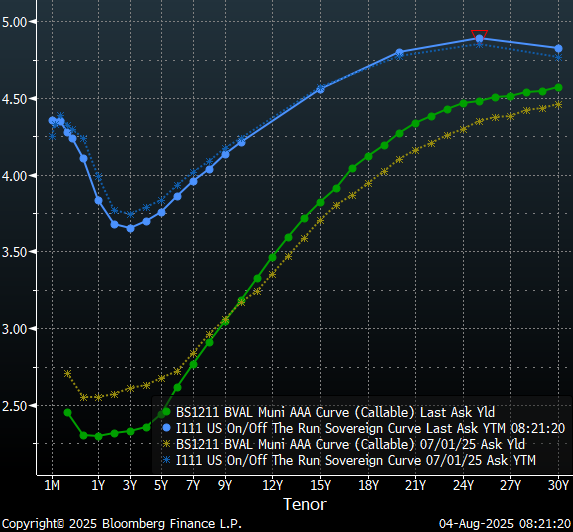

Throughout the month of July, both the Treasury and municipal yield curves experienced meaningful steepening. Munis steepened more than Treasuries, largely due to yields falling on the short-end of the curve rather than yields climbing on the long-end. For the Treasury curve, the steepening was less pronounced as 30-year yields climbed only 2.5 bps and yields around the 1-year mark dropped a significant 16bps. Currently, the municipal curve is at its steepest around the 10-year tenor with 51 bps of slope from 8 to 11-years. In addition, after this past week, the curve has steepened notably around the 5-year tenor with 33 basis points of slope from 4 to 7-years. Overall, the steepness of both curves provides significant incentive for duration extension.

Over the past week, muni/Treasury ratios have generally cheapened, particularly around the 10-year tenor. Over the past month, ratios in the longer intermediate and on the long-end have cheapened with short to short intermediate ratios a bit richer. Over the past month, the biggest changes have occurred around the 20-year tenor, which has gone from being in the high 80’s to the low 90’s. Over the past week, the biggest changes have been around the 10-year tenor as ratios approach 80%. Overall, the 10-year and 20-year portions of the curve are strategically appealing with a combination of compelling ratios and yield curve slopes that reward extension. However, past this point the yield curve discourages extension by flattening to just a basis point or two per year. As a result, extending out to the 20-year maturity allows investors to capture over 95% of the 30-year municipal curve.

This week, the municipal bond calendar includes more than $17 billion in new issues, according to data compiled by Bloomberg. Large issues on the calendar include: the City of New York, NY, which plans to sell $1.78b of bonds, Brightline Florida Holdings LLC, which is scheduled to sell $985 million, and Beth Israel Lahey Health Obligated Group, which plans to offer $930 million. In addition, there are 34 school districts in Texas planning to sell bonds backed by the Texas Permanent School bond guarantee fund. This supply will likely be met with strong demand following last week’s addition of $937 million by municipal bond mutual funds, as reported by LSEG Lipper Global Fund Flows. In addition, municipal bond redemptions and maturities are expected to be $21.6 billion in the next 30-days.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.

HJ Sims is proud to be attending and sponsoring at the 2025 NIC Fall Conference.

Attending:

Aaron Rulnick, Managing Principal

Curtis King, Executive Vice President

Brady Johnson, Senior Vice President

Brett Edwards, Senior Vice President

Brock Bagelman, Associate

{kind=link}

{kind=link}

{kind=link}