Overview

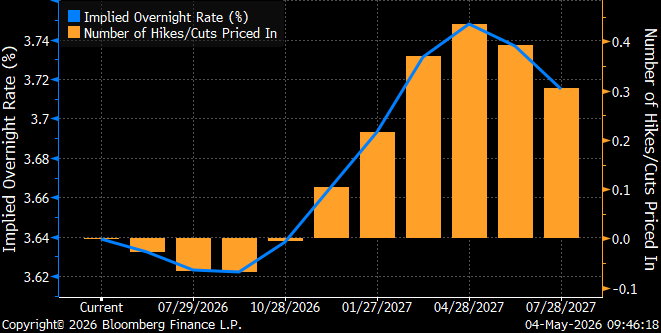

Last week the Fed voted to leave its policy rate unchanged at 3-1/2 to 3-3/4 percent citing developments in the Middle East as contributing to heightened uncertainty in their economic outlook. Although this was the Powell’s final meeting serving as Fed chair, he has announced his intentions to remain on the Fed’s board after his term as chair ends. Powell could potentially remain in place as a governor until that term ends in 2028. The Fed does not meet again until June 16-17, when Kevin Warsh will host his first meeting as the new chair.

It is notable that as the market transitions from Powell to Warsh, the outlook has shifted. At last week’s meeting, four Fed officials voted against the board’s decision with objections over language suggesting the central bank would eventually resume cutting rates. Rising oil prices and a lack of progress in talks between the US and Iran has markets concerned that rates will remain higher for longer. With the Fed’s dual mandate to promote maximum employment and stable prices, the markets are concerned that policymakers will focus on oil fueled inflation rather than employment. Although the Fed funds futures market is currently anticipating that rates remain unchanged for the next 12-months, the outlook has shifted from cuts to hikes.

Insights and Strategy

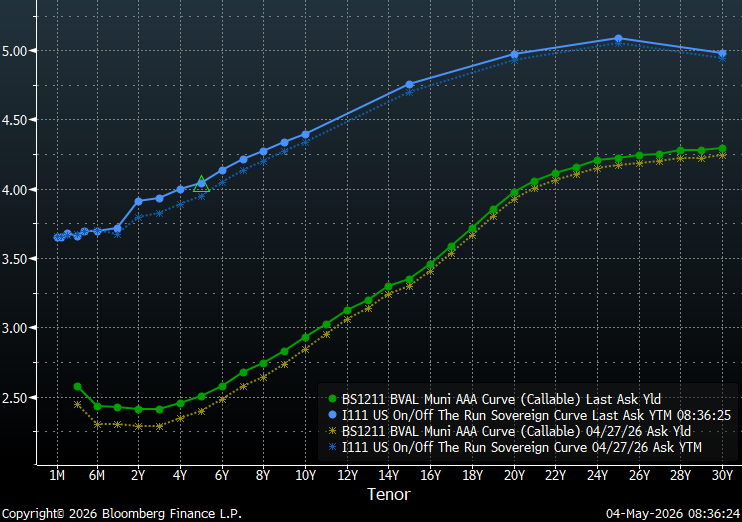

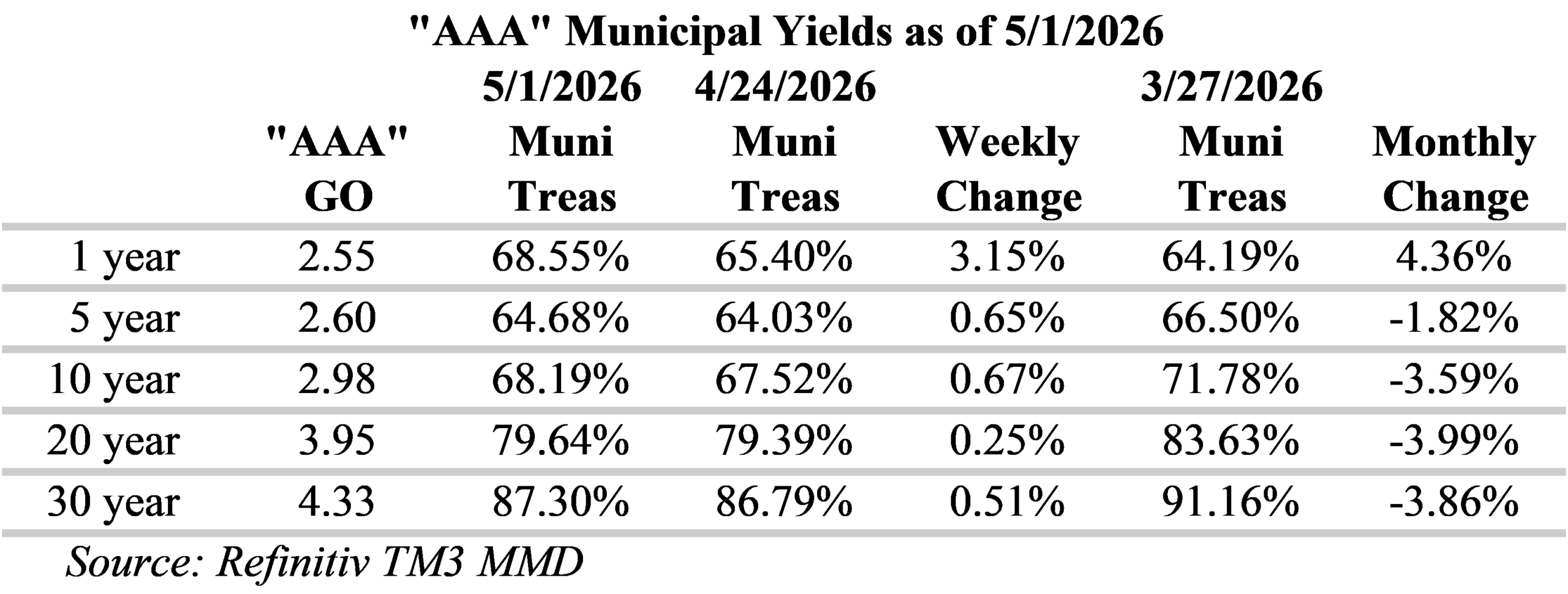

Over the past week, munis and Treasuries have both sold-off with rates rising anywhere from five to 13-basis points for all but the shortest maturities. The biggest changes have occurred around the policy sensitive two-to-three-year tenors while yields have risen about 5 bps for maturities past 14-years. Despite these developments, investors continue be rewarded for extending out the yield curve with the steepest yields in the 18-21-year maturity range. The long-end of the yield curve remains increasingly flat past 20-years, with a total slope of 26 bps from 21-30-years. Due to this flat tail, municipal bond investors can currently buy maturities around 20-years that yield over 90% of the 30-year curve.

As a result of the prolific short maturity bid-wanted activity, municipal/Treasury ratios for one-year and shorter maturities are meaningfully higher than they were last week with ratios over 3% higher/cheaper. Past five years, ratios slip a bit higher with demand extending out the curve to the longer maturities where relative yields are more appealing. However, municipal bonds have fallen just below several important reference points along the curve. Ratios for 10-year municipal yields remain under 70% of Treasuries, 20-year ratios are below 80% and 30-year ratios are below 90% of Treasuries. For investors seeking to maximize curve positioning with relative value, the 18 to 21-year part of the municipal yield curve has become tempting with slopes of 12 to 13-bps per year. Although ratios past 20-years remain attractively priced relative to Treasuries, the yield curve is very flat and does not reward extension over these longer tenors.

The Municipal new issue calendar picks-up a bit this week as US state and local governments are expected to sell over $12 billion of bonds. Notable deals include: the City of Chicago Waterworks Revenue Bonds with $824.7 million, Texas State University System has scheduled $762.2 million, Chabot-Las Positas Community College District is expected to offer $531 million, and Indiana Municipal Power Agency is anticipated to bring $430 million to the market. Despite record issuance this year, technical conditions remain supportive of the primary market. Last week, municipal bond investors added approximately $615 million to municipal-bond funds, according to LSEG Lipper Global Fund Flows. Furthermore, May tax-exempt reinvestment proceeds are expected to reach approximately $34.5 billion.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.