Overview

Despite the headlines and anxiety leading up to last week’s supreme court ruling, which determined the reciprocal tariffs are illegal, the bond market’s response was fairly measured. The Treasury market initially reacted with longer dated yields jumping approximately 6 basis points to 4.75%, before settling back as more information emerged. The muted response was partly due to the markets anticipating the ruling by pricing-in the outcome in advance and partly due to the potential for replacement tariffs. However, there remains significant uncertainty about when, or if, the billions in collected tariffs will be refunded. Should the tariffs be refunded, the bond market currently anticipates the burden will be shifted to Treasury issuance and result in higher yields.

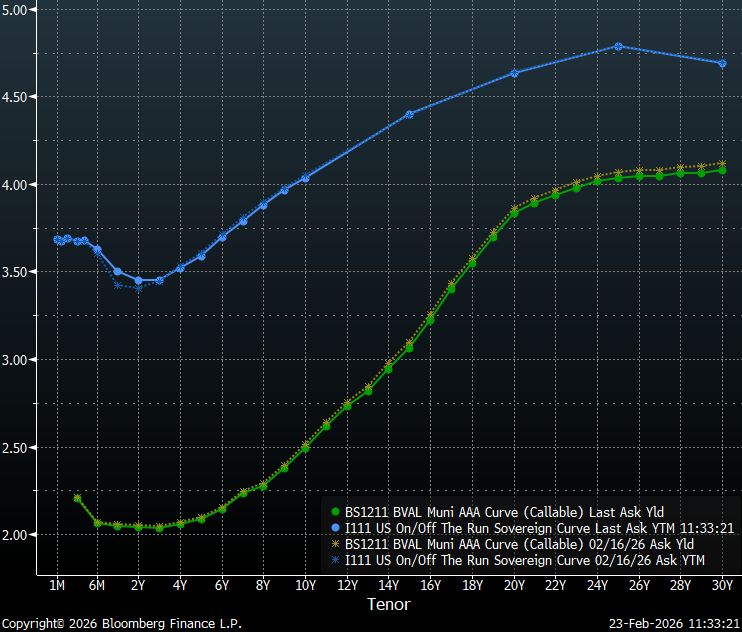

Last week both the municipal bond market and the Treasury market were little changed. Munis rallied three to four basis points on the long-end of the yield curve as $14 billion in mid-month principal payments poured in during a shortened holiday week. Treasuries were essentially unchanged, with adjustments primarily around the policy sensitive two-year tenor. Slopes along the municipal yield curve remain consistently steep from 10 to 20-years, with 137 bps of slope compared to 46 bps from 1 to 10-years and 34 bps from 21 to 30-years.

Insights and Strategy

Currently, Investors benefit from positioning in the intermediate/longer portion of the yield curve. In addition, a steep roll-down over time is drawing investors out the curve with some protection against rising rates. Due flattening past 20-years, municipal bond investors can currently buy maturities under 20-years that yield almost 90% of the 30-year curve. With muni/Treasury ratios for 10-year and shorter maturities quite rich at under 60% of Treasuries, extending maturities further out the curve has the added benefit of more appealing relative yields. Ratios in 20-year and longer maturities remain attractive, relative to Treasuries, due to seasonal activity and wider spreads. However, the yield curve remains very flat over these longer tenors. For investors seeking to maximize curve positioning with relative value, the 17 to 20-year part of the municipal yield curve has become very tempting with slopes of 15 to 16-bps per year.

The municipal new issue calendar expands this week to $10.6 billion of new issues. Notable issues include: the University of California with $2.0 billion of bonds, Lee County Florida is scheduled to sell $681.3 million in airport revenue bonds, and the Santa Clara Financing Authority is expected to sell a $396.3 million issue. This week’s deals should see a strong reception following 13 consecutive weeks of inflows, with approximately $1.3 billion being added to municipal bond funds last week alone, according to LSEG Lipper Global Fund Flows. Considering current muni/Treasury ratios, it is not surprising that the majority of inflows are going to intermediate and long-term muni funds, which reportedly received over $1 billion last week.

Herbert J. Sims & Co. Inc. is a SEC registered broker-dealer, a member of FINRA, SIPC. The information contained herein has been prepared based upon publicly available sources believed to be reliable; however, HJ Sims does not warrant its completeness or accuracy and no independent verification has been made as to its accuracy or completeness. The information contained has been prepared and is distributed solely for informational purposes and is not a solicitation or an offer to buy or sell any security or instrument or to participate in any trading or investment strategy, and is subject to change without notice. All investments include risks. Nothing in this message or report constitutes or should be construed to be accounting, tax, investment or legal advice.